Perspectives on the economic outlook have become increasingly mixed over the past year. Underlying the prevailing narrative of a moderating economy is a heightened level of disagreement between firms about their views on hiring and consumer demand, among other indicators of business conditions. For some firms, conditions are clearly deteriorating, while others report ongoing growth and optimism. The source of this disagreement is varied as well. In certain sectors of the economy, the disagreement stems from changes in consumer preferences and habits. For other sectors, a dichotomy has emerged due to the types of customers that businesses are able to attract. Many firms are divided by their degree of exposure to geopolitical risk. This diversity in perspectives translates to a heightened reallocation of activity across competing firms as some businesses gain market share at the expense of others.

The highly mixed anecdotal reports are corroborated by data collected through surveys conducted by the Kansas City Fed. The variation in responses to a variety of questions about current and future business conditions can be aggregated into a single quantitative measure of disagreement that provides meaningful information about broader economic conditions. In this edition of the Rocky Mountain Economist, we describe the recent rise of disagreement among firms and why it matters to the regional economy. Historically, periods of high disagreement tend to lead to softening in employment conditions. With disagreement currently at a highly elevated level, we could see similar implications for the path of the regional economy, particularly regarding employment growth.

Disagreement among firms is historically high

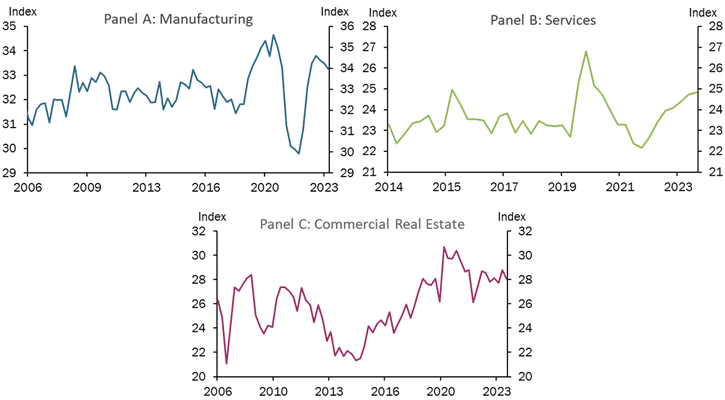

The past year has been characterized by elevated levels of disagreement spanning across industries and economic indicators that typically move together. Chart 1 Panels A, B and C depict a measure of disagreement derived from the Kansas City Fed surveys for the Manufacturing, Services and Commercial Real Estate sectors, respectively. The surveys interview contacts across the Tenth District region (Colorado, Kansas, Missouri, Nebraska, Oklahoma, New Mexico, and Wyoming) about their views on present and future business conditions.i Respondents characterize changes in activity – such as hiring activity, capital expenditures or customer demand – indicating if activity is moving up “up”, “down” or showing “no change” for various aspects of their businesses. The lack of uniformity of answers allows for a calculation of “disagreement,” which provides a measure of the mixedness of responses that varies over time.ii Essentially, if most responses are skewed toward a single answer, then disagreement is low. However, if there is a more even mixture in the responses about certain activities across firms, then disagreement is characterized as high.

Panel A shows that disagreement among manufacturing and services firms is at historically high levels, second only to the first half of 2020 when regional firms were responding to the economic upheaval caused by the COVID-19 pandemic. In 2020, businesses’ outlooks were conflicting as the level of disruption to their operations due to public health mandates differed vastly among firms. Shifting consumer demand toward essential items, supply chain disruptions, travel restrictions and access to federal assistance, among other factors, created diverse experiences for firms. Beginning in the first quarter of 2021, disagreement fell precipitously to reach a historic low level in early 2022. Firms across industries characterized economic conditions more similarly as most businesses were in agreement about the resumption of economic activity and accelerated price growth during that period. Disagreement began to rise again throughout 2022 in both service and manufacturing sectors and is currently elevated to near historic highs. Businesses in various aspects of the commercial real estate industry are similarly expressing high levels of disagreement, highlighting the pervasive nature of this feature of the economy (Panel C).

Chart 1: Disagreement is high in a variety of sectors

Sources: Kansas City Fed Surveys, staff calculations

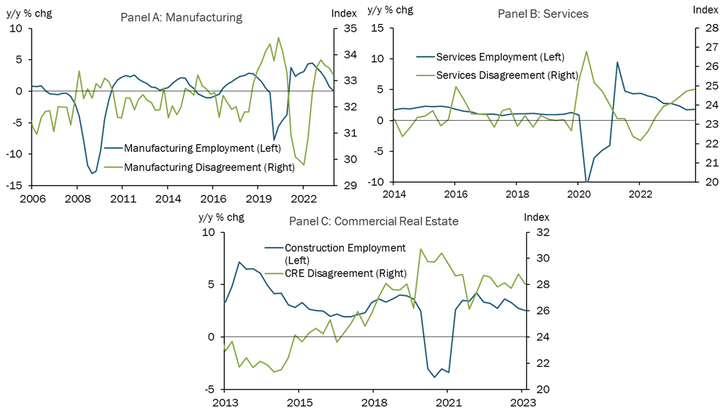

High disagreement is associated with slowing employment growth

Disagreement among businesses is not mere noise about the outlook as it provides a signal about the ebbs and flows of employment growth for industries. Chart 2 shows that in the manufacturing and services sectors, periods of high disagreement tend to coincide with softening labor demand, whereas periods of low disagreement are accompanied by employment growth. The manufacturing sector demonstrates this relationship often, as its business cycle dynamics are more pronounced. The services sector had quite flat employment growth between 2014 and 2019, and also relatively flat levels of disagreement. But in 2020, the same pattern of employment softening amid a period of high disagreement emerged (Panel B). Commercial real estate industry contacts reported low levels of disagreement during the period between 2013 and 2016. However, construction employment began to soften in 2017 as disagreement rose steadily from its previous low level. The current high level of disagreement across all industries is associated with some broad slowing of employment growth recently, though growth has yet to turn negative. However, continued elevated disagreement may suggest that further softening is ahead.

The negative relationship between disagreement and employment is quite intuitive. Emerging differences in views can signal a turning point in economic conditions. When economic conditions first become more adverse, some firms contract and reduce their production and demand for labor while others are more insulated, or even expand by absorbing market share. Evidence in Chart 2 shows that it is not typical for all businesses to deteriorate in conditions simultaneously, which would result in low disagreement coinciding with declines in growth. Conversely, periods of expansion or normal growth, reflect a greater stability and consensus among businesses about economic conditions.

Chart 2: Levels of disagreement are high during periods of softening employment

Source: Kansas City Fed Survey, BLS, Haver Analytics, staff calculations

Disagreement is a useful measure of signal quality

Anecdotal reports featured in the Tenth District Beige Bookiii shed further light on the disparities in perspectives that underly the heightened level of disagreement. For example, changes in consumer spending habits have created disagreement among retailers. In February, non-discretionary retailers such as grocery stores reported strong demand whereas businesses selling discretionary items such as clothing and personal care stores report softening demand due to consumers’ increased price sensitivity. Additionally, due to a shift in travel habits, hotels that cater more to leisure travelers are seeing less growth in activity whereas hotels catering to large events and business travel are reporting greater strength in occupancy. For others, business activity is split across the types of contracts that businesses are able to obtain. Last November, manufacturers reported that the presence or absence of government and defense contracts has created contrasting outlooks whereby firms that obtain these contracts are planning for relatively stronger capital expenditures. Still, others are divided by their degree of exposure to geopolitical risk. In February, businesses reported that their reliance on international shipping increased their exposure to shipping delays, whereas firms relying on domestic shipping benefited from the resolution of supply chain bottle necks. These reports reveal that opposing views are an important feature of regional economic activity at the moment.

__________

i For more information on the Kansas City Sed Surveys see: https://www.kansascityfed.org/surveys/

ii Formally, the disagreement is calculated as the level of Shannon Entropy for all survey respondents and questions. For more details see the explanation in Greene and Sly (2024) that applies this methodology to the commercial real estate sector for the KC Fed Region.

iii For additional anecdotal reports from the most current release of the Tenth District Beige Book see: https://www.kansascityfed.org/surveys/beige-book/