The U.S. economy is in its 114th consecutive month of expansion following the severe 2007-09 recession, marking this recovery as the second longest on record. For more than eight years, labor market conditions have been improving gradually, and many labor market indicators are approaching, or have surpassed, pre-recession levels. As a result of these significant improvements, available workers have become harder to find, leading many to view current labor market conditions as tight. This issue of the Rocky Mountain Economist analyzes key labor market indicators and compares current and historical levels to assess how tight current labor markets are in Colorado, New Mexico and Wyoming.

Unemployment

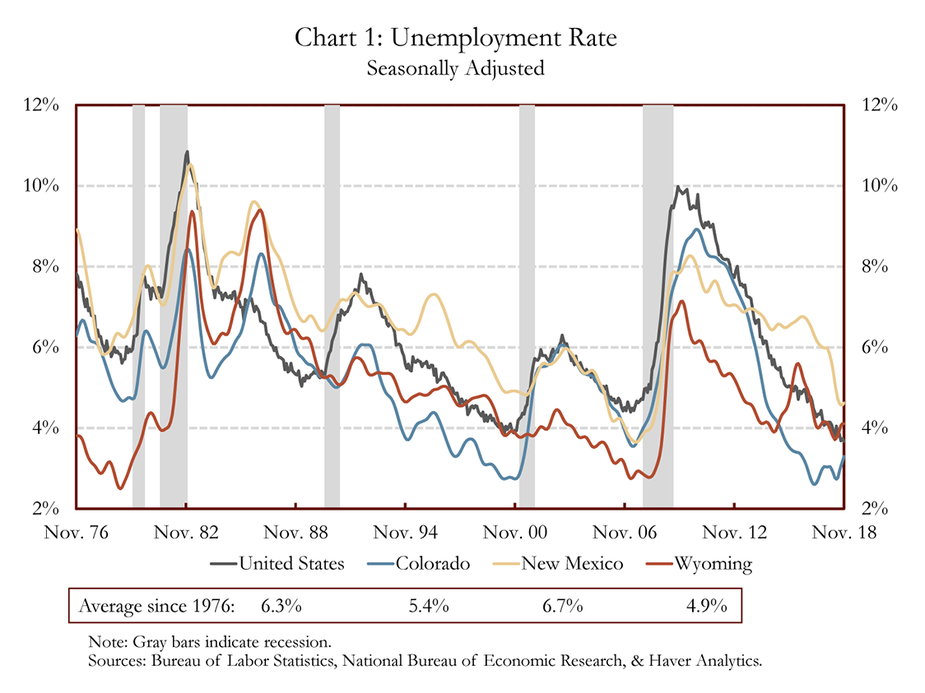

The unemployment rate is one of the most frequently cited measures of labor market conditions.i Unemployment typically rises during recessions as people lose their jobs and new labor market entrants struggle to find work, and falls during expansions as firms hire employees in greater numbers.ii Unemployment rates can differ greatly across states due to factors such as demographics, education levels and industry composition. During the 2007-09 Great Recession, unemployment rates rose sharply in the United States and the Rocky Mountain States (Chart 1).iii Colorado’s unemployment rate reached 8.9 percent, surpassing its previous peak from the mid-1980s. Unemployment rates in the United States, New Mexico and Wyoming also increased significantly but remained below their peaks in late 1982 and early 1983. However, the peak national unemployment rate of 10 percent over the Great Recession exceeded the rate reached in each of the Rocky Mountain States over the same period.

Over the past eight years, unemployment rates have fallen gradually from their recession highs, and current unemployment rates in the United States, Colorado, New Mexico and Wyoming now are below their historical averages (listed under the legend in Chart 1). Additionally, Colorado’s unemployment rate of 2.6 percent in spring 2017 was the lowest since recording began in 1976, while the national unemployment rate of 3.7 percent in fall 2018 was the lowest since 1969. In addition to following the national business cycle, New Mexico and Wyoming’s high reliance on the energy sector frequently leads to higher unemployment rates during energy sector downturns, such as in the mid-1980s and late-2014.iv Although unemployment rates have declined considerably since 2011 and are below historical averages, rates in New Mexico and Wyoming remain above pre-recession levels.

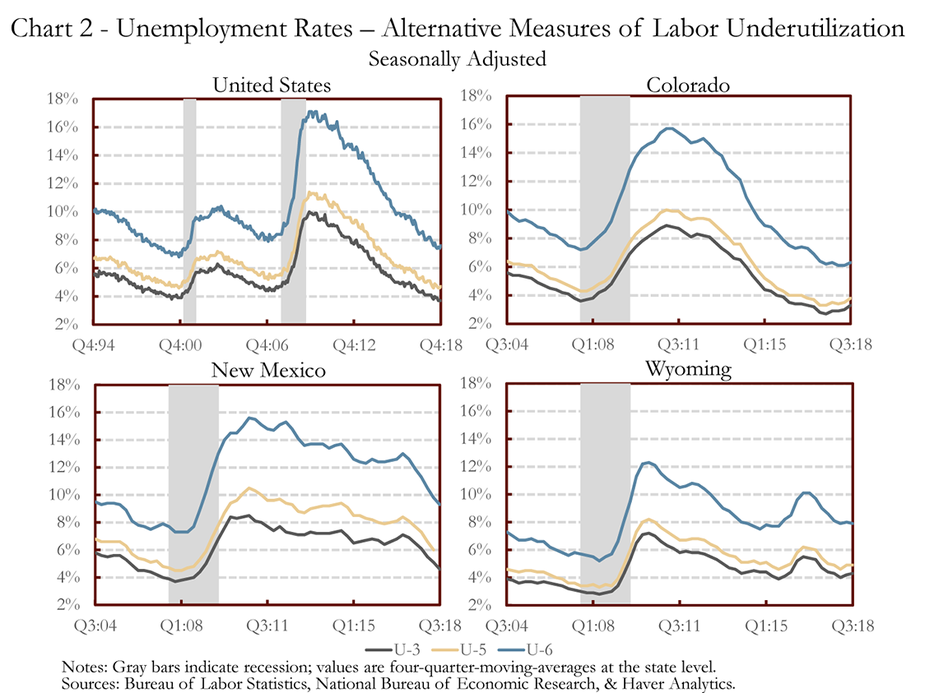

The Bureau of Labor Statistics (BLS) provides several measures of unemployment in addition to the unemployment rate shown in Chart 1 (termed U-3 by the BLS). Two alternative measures of unemployment, the U-5 and U-6 unemployment rates, provide additional insights about the effects of the Great Recession on labor markets by expanding the definition of unemployed. In addition to the unemployed workers included in the previously defined U-3 rate, the U-5 unemployment rate includes individuals who are marginally attached to the labor force. Marginally attached individuals are defined as those who have not actively looked for work in the past four weeks but have searched for work in the past 12 months and want and would take a job. The U-6 unemployment rate includes unemployed individuals, marginally-attached individuals and those working part time who would rather have a full-time job.v

The U-5 and U-6 unemployment rates increased significantly during the Great Recession as some individuals had trouble finding jobs and stopped actively looking for work while others could only find part-time employment (Chart 2).vi The number of marginally attached and part-time workers has fallen from recessionary highs, and these unemployment rates are now below their pre-recession levels at the national level and in Colorado.

Future gains in employment can be fueled both by unemployed workers finding jobs and new entrants into the labor force. As unemployment rates continue to tighten, growth in the labor force will be a key source for employment growth as the next section discusses in detail.vii

Labor Force

The labor force, which is the sum of those who are employed and those who are unemployed but have actively sought employment within the past four weeks, is another important metric to consider when assessing labor market conditions.viii,ix A rise in the labor force helps foster economic growth as it indicates that more individuals are working or are actively seeking employment. One primary factor that contributes to labor force growth is population growth, and the U.S. population continues to expand, albeit at a slower pace than in previous decades.

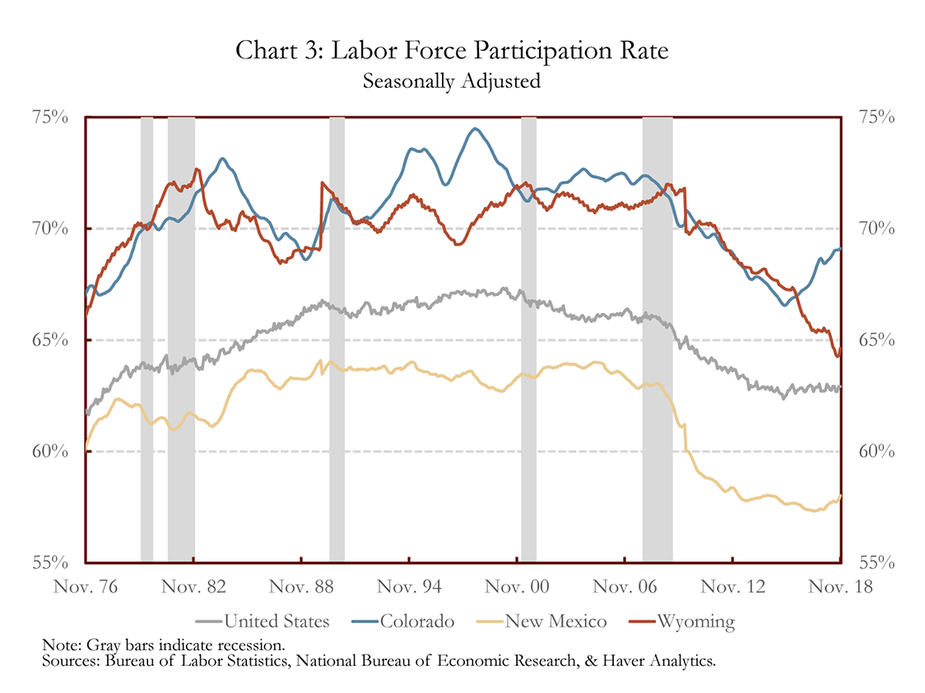

However, not everyone in the population chooses to be a part of the labor market, and therefore it is helpful to examine the share of the working age population that participates in the labor force, known as the labor force participation rate (Chart 3). Growth in the labor force participation rate indicates a larger labor force assuming that total population is not decreasing. The labor force participation rate in the United States grew steadily from about 1962 to a peak of 67.3 percent in early 2000, largely due to a growing number of women entering the workforce. Colorado and Wyoming also experienced growth in labor force participation rates through the turn of the century, although they experienced much more volatility due to effects from booms and busts in the energy sector, and for Colorado, the technology sector downturn in 2001. New Mexico’s labor force participation rate increased steadily until about 1990 and held steady near 63 percent until it began to decline around 2005.

Fewer job opportunities during the Great Recession led to declines in the labor force participation rate as many individuals dropped out of, or delayed entering, the labor force. For example, many younger individuals increasingly pursued education, delaying their entry into the job market. Other individuals may have lost jobs during the recession and then stopped looking for work after several unsuccessful attempts at finding a job. These factors reflect business cycle fluctuations and typically are short-term effects.

In addition to short-term business cycle fluctuations, participation rates also are affected by longer-term structural demographic changes. Most recently, many individuals of the large baby-boom generation have reached or are close to retirement age. This higher rate of retirements has put significant downward pressure on the labor force participation rate.x Between 2007 and 2017, an aging population explained the respective declines of about 83.8 percent, 98.6 percent, 60.7 percent and 40.9 percent in the labor force participation rates for the United States, Colorado, New Mexico and Wyoming.xi

During the recession, both short-term and long-term effects led to lower labor force participation rates. Amid improvement in labor market conditions, effects from business cycle conditions have turned positive. In recent years, these two trends roughly have offset each other, keeping the labor force participation rate roughly constant at the national level. Looking ahead, the combination of more job opportunities, fewer unemployed workers and rising wages may encourage some individuals on the sidelines to enter the labor force.xii However, it is likely that the long-term trend of retiring baby boomers will continue to put downward pressure on labor force participation rates as more individuals from this cohort, the youngest of whom are only 54, are expected to enter retirement over the next 10 years.

Therefore, any rise in labor force participation rates from younger generations may be offset, at least in part, by retirements from an aging population. This, combined with low unemployment rates and slow population growth, may slow future employment growth as there would be fewer available workers to hire. The next section discusses employment growth from the mid-1970s to today.

Employment Growth

Employment is an important indicator for tracking not only the health of the labor market, but that of the economy overall. Growth in the number of individuals employed indicates that firms are expanding their operations and that demand is increasing. Higher levels of employment also result in more individuals earning income, which can help boost consumer spending.

Job openings typically are filled by previously unemployed workers, new entrants into the labor force or workers who are taking on an additional job. As labor markets tighten, employment growth starts to be constrained by the number of available workers for hire. There already is some evidence of this as the number of unemployed persons nationally has fallen below the number of job openings.xiii If unemployment rates remain low and labor force participation rates hold roughly steady, employment growth may begin to slow as firms struggle to fill open jobs.

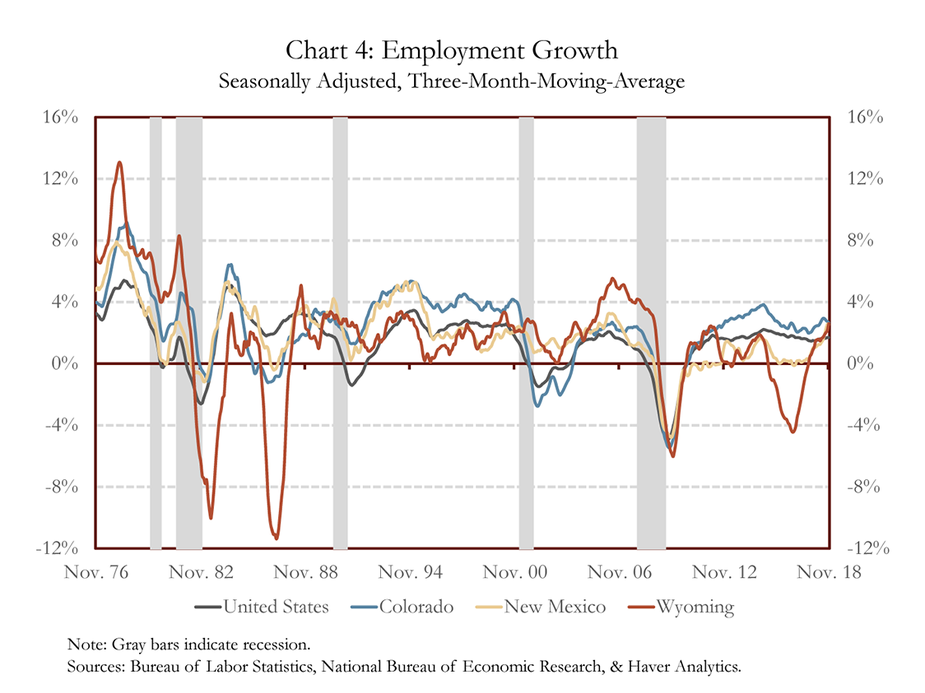

Historically, employment growth in the Rocky Mountain States tends to follow the national business cycle (Chart 4). However, employment in Colorado was affected more than the nation by the surge and subsequent bust in the technology sector in the late-1990s and early-2000s. Similarly, Wyoming’s employment is more heavily affected by booms and busts in the energy sector.xiv

In recent years, Colorado has enjoyed faster employment growth than the nation, as the state’s economy has recovered at one of the fastest paces across the country. New Mexico and Wyoming’s employment has grown at a slower pace in recent years due to some out-migration as well as slower overall economic growth due, in part, to the downturn in the energy sector.

From each state’s pre-recession peak employment to its trough during the recent downturn, Colorado, New Mexico and Wyoming lost 155,300; 52,300; and 19,500 jobs, respectively. Over the past eight years, employment in Colorado has increased at an annualized rate of about 2.5 percent and added 543,600 jobs in total, resulting in employment well above pre-recession levels. In contrast, New Mexico has grown at a more modest rate, about 0.8 percent annually, and just passed its 2008 peak in September 2018. Employment in Wyoming remains about 9,700 jobs less than its 2008 peak, due to job losses during the 2007-09 recession and the late-2014 downturn in the energy sector.

Over the past year, employment growth has been strong in the Rocky Mountain States, with each state expanding at a faster pace than their average growth since 1976. Looking ahead, the pace of employment growth is heavily dependent on the amount of available labor. As labor markets continue to tighten, employment growth may naturally slow as there would be fewer individuals available to fill open jobs.

Conclusion

Following a sharp deterioration in labor market conditions during the 2007-09 Great Recession, labor market conditions have improved over the past eight years. Historically low unemployment rates suggest that labor markets now are tight in many areas of the country. In addition, an aging workforce may continue to put downward pressure on labor force participation rates. These factors may limit future employment growth as fewer individuals would be available to fill open positions.

Despite low unemployment rates, wage growth has been modest during the recent expansionary period. Analysts have proposed several possible explanations including shifts in industry mix, changes in worker demographics, wage rigidity during the recession and higher benefits costs.xv, xvi, xvii However, wage growth has picked up more recently and is expected to accelerate as labor markets continue to tighten.

End Notes

i The term “unemployment rate” refers to the U-3 unemployment rate as defined by the Bureau of Labor Statistics here External Linkhttps://www.bls.gov/lau/stalt.htm, unless otherwise noted.

ii A person is only counted as unemployed if they are 16 or older and have actively looked for a job within the past four weeks. Those too young to work, retired or who are simply not looking for a job nor want one are not included in the labor force. Movement in the unemployment rate can thus be explained by changes in the number of those unemployed, the size of the labor force, or both.

iii Unemployment rates for the United States were reported monthly beginning in 1948, but individual states did not begin recording on a monthly basis until 1976. New Mexico and Wyoming saw significant increases in unemployment rates in the late 1970s through the mid-1980s, although this was over the course of two recessions.

iv Colorado also had a higher reliance upon the energy sector during the mid-1980s, as evident by its increase in unemployment rates around these energy-sector busts.

v Bureau of Labor Statistics, External Linkhttps://www.bls.gov/lau/stalt.htm

vi Data for the U-5 and U-6 began in 1994 for the United States, and 2003 for Colorado, New Mexico and Wyoming.

vii In addition to the number of unemployed, the unemployment rate also is dependent on the labor force. For example, an increase in the unemployment rate can be caused by an increase in the level of unemployed, and/or a decrease in the labor force.

viii In line with the definition of unemployment provided in the first section, unemployed persons refers to the U-3 definition of unemployment.

ix Technically, the labor force is the level of the civilian noninstitutionalized population age 16 and older. Additional information on labor market component definitions can be found on the Bureau of Labor Statistics’ website: External Linkhttps://www.bls.gov/bls/glossary.htm#L

x Baby boomers commonly are defined as those born between 1946 and 1964.

xi For additional information on how the decline in labor force participation rates can be attributed to aging, the Rocky Mountain Economist article from the first quarter of 2014 dives deeper into this topic.

xii Recent research also has indicated that individuals who engage in informal work—such as driving for ride-share programs, sometimes referred to as being the “gig economy”—are not consistently included in labor force participation rates due in part to irregular work schedules and reporting error. With this, if informal work arrangements continue to proliferate, it is possible that the labor force participation rate will slightly understate the actual rate of working individuals. For more information on the topic, see Who Counts as Employed? Informal Work, Employment Status, and Labor Market Slack from the Federal Reserve Bank of Boston website: https://www.bostonfed.org/publications/research-department-working-paper/2016/who-counts-as-employed-informal-work-employment-status-and-labor-market-slack.aspx

xiii Using data from the Job Openings and Labor Turnover Survey from the Bureau of Labor Statistics, it is estimated that as of August 2018, there were more than 1 million more job openings than number of unemployed persons.

xiv Current Employment Statistics - Bureau of Labor Statistics, Haver Analytics, and authors’ calculations.

xv For additional information on how shifts in industry mix have impacted wage growth, the Rocky Mountain Economist article from the first quarter of 2015 dives deeper into this topic.

xvi For additional information on how changes in worker demographics and higher benefits costs have impacted wage growth, see How Much Are Workers Getting Paid? A Primer on Wage Measurement from the Council of Economic Advisers: External Linkhttps://www.whitehouse.gov/wp-content/uploads/2018/09/How-Much-Are-Workers-Getting-Paid-A-Primer-on-Wage-Measurement-Sept-2018.pdf

xvii For additional information on how wage rigidity impacted wage growth, see The Path of Wage Growth and Unemployment from the Federal Reserve Bank of San Francisco: External Linkhttps://www.frbsf.org/economic-research/publications/economic-letter/2013/july/wages-unemployment-rate/