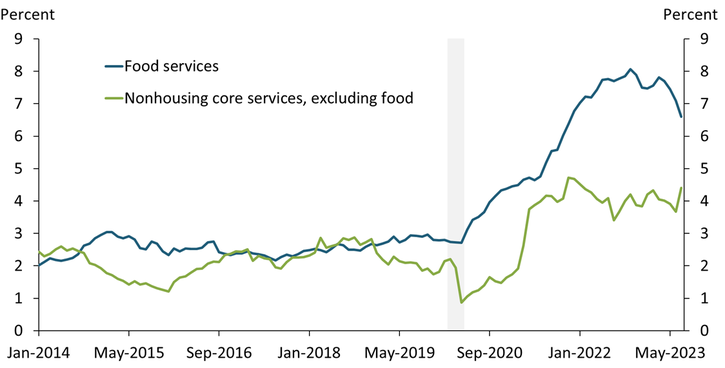

Headline inflation—as measured by the price index for personal consumption expenditures (PCE)—has slowed in recent months, but inflation for core services has remained elevated. One reason for sustained inflationary pressure in core services has been high inflation for food services, a category that includes spending at restaurants and other food service establishments._ Chart 1 shows that food services inflation has outpaced other nonhousing core services inflation by an average of almost 3 percentage points since the end of the COVID-19 recession._ From July 2022 to July 2023, prices at restaurants and other food service establishments increased by 6.5 percent. Food services account for about 10 percent of core services excluding housing. Accordingly, continued high inflation for food services has put upward pressure on inflation for nonhousing core services.

Chart 1: Twelve-month food services inflation has been higher than inflation for other core services (excluding housing)

Note: Gray bar denotes National Bureau of Economic Research (NBER)-defined recession.

Sources: U.S. Bureau of Economic Analysis (BEA) and NBER (both accessed through Haver Analytics).

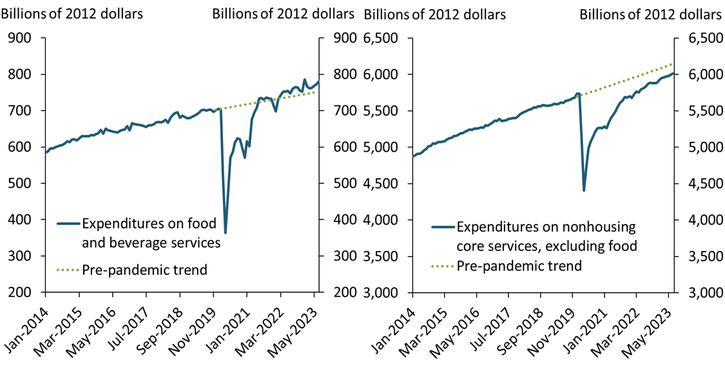

What is driving high inflation in food services? Strong demand since the pandemic, ongoing labor shortages, and higher-than-average wage growth in the sector all have likely played a role. On the demand side, Chart 2 shows that real spending on food and beverages rebounded faster to its pre-pandemic trend than spending on other nonhousing core services. The faster rebound may be attributed to the vaccine rollout, pent-up demand for dining out, and the many fiscal stimulus programs during the pandemic recession (Adjemian, Li, and Jo 2023). Although monetary policy has tightened substantially since the pandemic, and the financial strength of households has started to moderate, spending on food services has remained strong and above its pre-pandemic trend.

Chart 2: Spending on food services rebounded faster than spending on other nonhousing core services

Sources: BEA (Haver Analytics) and authors’ calculations.

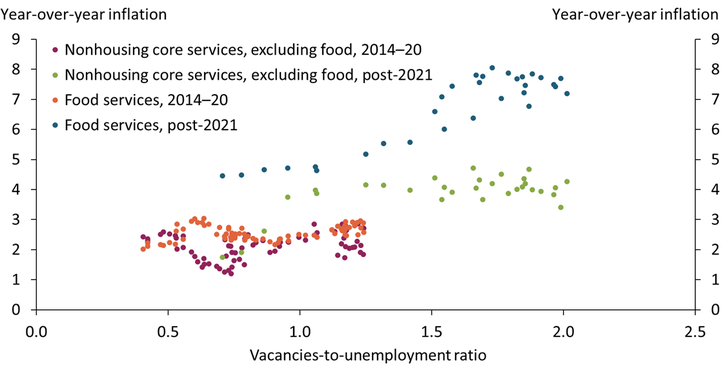

In addition, inflation for food services appears to have become more responsive to labor market shortages than other services. Chart 3 shows that year-over-year inflation for food services and other nonhousing core services had a similarly positive—but somewhat weak—relationship with labor market tightness from 2014 to 2020. After 2021, however, when labor markets became severely tight, food services inflation increased faster than inflation for other core services.

Chart 3: Food services inflation has become more responsive to labor market tightness

Sources: BLS and BEA (both accessed through Haver Analytics).

Tight labor markets can drive up food services prices by significantly raising restaurants’ labor expenses and reducing their capacity to serve customers. According to the U.S. Department of Agriculture’s Economic Research Service, 75 cents out of each dollar spent on food away from home are incurred by food services; the other 25 cents are incurred by food processing, wholesale trade, and other parts of the supply chain. Shortages of workers in restaurants and drinking places can be inflationary, as they rely heavily on labor to produce services. Moreover, the National Restaurant Association estimates that 66 percent of restaurant’s costs are tied to labor and food costs, and Cowley and Scott (2022) argue that the price of food and food processing is disproportionately related to labor costs._

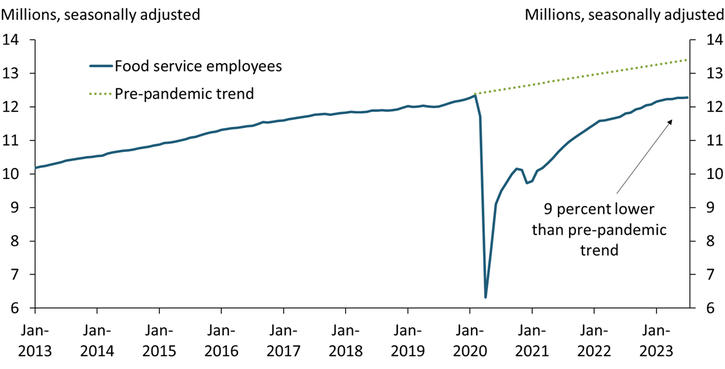

Labor market tightness contributed to a shortage of workers in the food services industry. Chart 4 shows that the number of employees in food and drinking places was 9 percent below its pre-pandemic trend as of July 2023. Together, labor shortages in the industry and high demand for food services led employee earnings to grow more quickly than in other industries. Since 2020, food services workers have experienced more than 7 percent annualized growth in earnings, compared with only 4.6 percent annualized growth for workers in other services industries. Food processing workers have also seen higher earnings growth (more than 5.7 percent annualized), suggesting labor shortages and higher labor costs are indeed putting upward pressure on food services inflation.

Chart 4: Food services seem constrained by labor shortages

Source: BLS (Haver Analytics).

Food services account for a nontrivial share of nonhousing core services to households, and inflation in the sector remains significantly higher than inflation for other core services. A fast rebound in spending and substantial labor market constraints may explain the divergence, as businesses in the food services sector rely disproportionately on labor to produce output. Labor shortages appear to have hindered the capacity of the sector to meet demand for food services. Ultimately, constraints on labor have led to high wage growth in the sector, high cost pressures, and high food services inflation (Shapiro 2023; National Restaurant Association 2022). Lowering food services inflation will likely require either a drop in demand for food services, an increase in labor supply, or an increase in labor productivity.

Endnotes

-

1

Food purchased at a grocery store for at-home consumption is considered a good in both the consumer prices index (CPI) and personal consumption expenditures (PCE) index. However, the categorization of food purchased at restaurants, or away from home, differs between the CPI and PCE. Food away from home is considered a good in the CPI but a service in the PCE price index.

-

2

We exclude food furnished for employees from our measures of food services to focus more closely on the decision of households. The measure that we use is spending on purchased meals and beverages from food sold in retail, services, and leisure and accommodations establishments. This measure of spending includes tips and incorporates spending on food on-premises (for example, in a restaurant) and off-premises (such as takeout). We exclude housing services inflation from our measures of core services inflation to better capture trends in the data. Housing services inflation tends to be less useful in explaining services inflation in the future than nonhousing core services inflation. Housing services inflation adjusts somewhat slowly after an economic shock because new lease contracts roll over old lease contracts. Therefore, housing and rent repricing dynamics tend to lag repricing of other goods and services.

-

3

We present further evidence in the supplementary material that an increase in the price of agricultural commodities has limited effect on the price of food services. The exercise suggests that costs along the food supply chain may have a larger effect on the price of food than higher commodity prices.

References

Adjemian, Michael K., Qingxiao Li, and Jungkeon Jo. 2023. “External LinkDecomposing Food Price Inflation into Supply and Demand Shocks.” Working paper, July 12.

Cowley, Cortney, and Francisco Scott. 2022. “External LinkCommodity Prices Have Limited Influence on U.S. Food Inflation.” Federal Reserve Bank of Kansas City, Economic Bulletin, September 23.

National Restaurant Association. 2022. “External LinkInflation Is Straining Restaurant Operations.”

Shapiro, Adam Hale. 2023. “External LinkHow Much Do Labor Costs Drive Inflation?” Federal Reserve Bank of San Francisco, Economic Letter, no. 2023-13, May 30.

U.S. Department of Agriculture Economic Research Service. 2023. “External LinkFood Dollar Application.”

Francisco Scott is an economist at the Federal Reserve Bank of Kansas City. Cortney Cowley is a senior economist at the bank. The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.