Summary

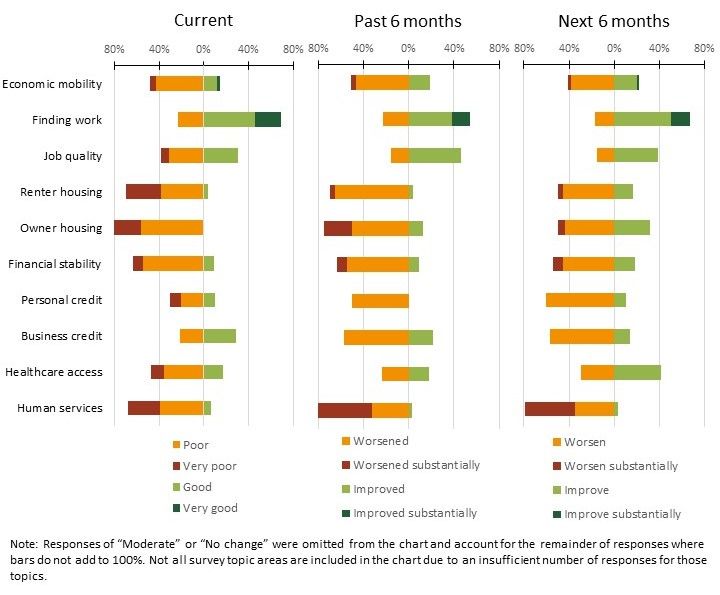

Community conditions in the Tenth District generally declined over the last six months, despite continued strength in the ability of low- and moderate-income (LMI) individuals to find work (Chart 1). Conditions for economic mobility, housing, personal finance, small business credit and human services were reported as poor, with housing-related contacts especially downbeat. Survey respondents had some optimism for the future, particularly around employment and healthcare access. However, most respondents were expecting worsening conditions in most sectors over the next six months.

Economic mobility outlook

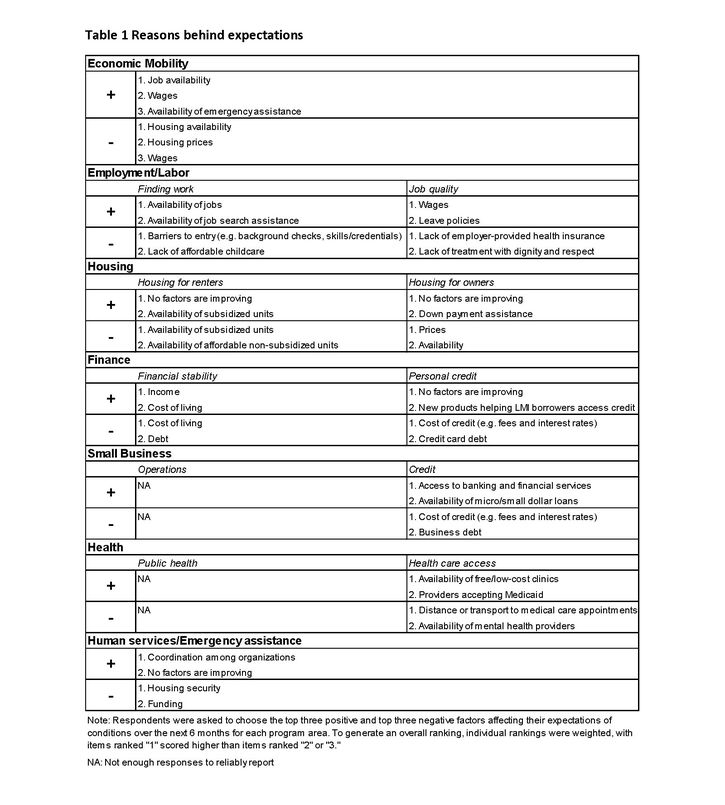

Responses were mixed on how conditions for economic mobility—an indicator of overall LMI conditions-may change over the next six months. Jobs and wages were the primary positive drivers for future economic mobility, while housing prices and availability were cited as the biggest drags (Table 1). More than a third of all respondents commented on affordable housing issues in an open-ended question on economic mobility, with particular concerns expressed about prices, quality, availability and lack of housing assistance. Even though housing has been a consistent area of strain in recent years, negative housing mentions in comments were up considerably from previous unpublished surveys.

Sector highlights:

- Employment: Respondents expect the job market to continue providing opportunities to find work. However, there were substantial concerns about many LMI individuals being able to attain those jobs. Respondents attributed this to increasing barriers to entry (increased use of background checks and drug screening) and the difficulties of getting to available jobs because of the cost or availability of transportation.

- Housing: Housing continued to be a substantial pain point. Respondents had very little optimism about affordability and accessibility improving in the near future. However, there were a few respondents who expect some improvements in owner housing, likely related to expectations that mortgage rates will decrease.

- Personal finance: Respondents attributed much of LMI households’ difficulty with financial stability to the increase in costs in recent years outpacing their ability to afford the increased cost of their basic needs. Meanwhile, there were growing concerns with the increasing cost of credit as more households utilize credit cards or turn to alternative financial services like payday loans.

- Small business: Small business credit had mixed responses, but nearly all respondents expressed difficulties for LMI small business owners as banks tighten lending standards. Several respondents mentioned a growing fear among business owners that they will have to close due to difficulty securing credit and various financial pressures and decisions they hoped to alleviate, at least temporarily, through credit.

- Healthcare: Many health organizations expect improvements in healthcare access over the next six months, related to the availability of free or low-cost clinics. However, structural issues around availability of mental health providers and transportation to providers were reported as considerable challenges by all health respondents.

- Human services: Respondents reported continued growth in demand for their services. Shelter was by far the most reported issue. One respondent framed it as, “The shelters are fuller than ever with no family spaces available. Motel and prevention funds are few. If we don't stop the stream of newly homeless households, we will be fighting an elusive and unstoppable wildfire of poverty.” Respondents also reported declining donations on top of trying to adjust to the loss of pandemic-era funds.

Chart 1: Community Conditions

What are the biggest difficulties that organizations are facing?

Respondents pointed to funding and fundraising, rising expenses and difficulty meeting demand for their services as the biggest difficulties that their organizations are facing. Staffing also was a highly ranked issue, but organizations linked it strongly to their ability to meet demand for their services. A large number of respondents stated that organizations had substantial difficulties filling open positions and keeping staff, which has impacted their ability to meet growing demand. Many organizations said they had funds to provide additional services, but their staffing difficulties have constrained their ability to expand offerings.

Organizations’ funding, staffing, ability to meet demand for their services and rising expenses all were strongly linked. As one organization stated, “We grapple with the ongoing challenge of securing sustainable, long-term funding for our organization. While the demand for our services is steadily increasing, we face difficulties in funding our programs. In response to the rising needs and attendance, we recently hired additional staff, even though we're not certain about the funding source for this position. While we have enough funds to operate for a couple of years, our primary focus and concern revolve around the sustainability of funding.”

Many organizations stated they were unable to fund their staff at competitive levels, hampering their ability to attract and keep staff. This was in addition to several respondents stating that wages are further constrained because of growing costs related to rent for their spaces, property and health insurance, and provision of services such as food. Adding to their difficulties were substantial reporting requirements by grant agencies as well as far fewer unrestricted funding opportunities than during the COVID-19 pandemic, which has led to significant gaps in the services they can offer.

About the survey

The 2023 Fall Community Conditions Survey (CCS) was conducted from Oct. 30 to Nov. 17, 2023, and received 98 responses from the 290 surveys sent (a 34% response rate).

The CCS goes to intermediary organizations with programming targeted to LMI populations. All survey respondents were asked to answer questions on conditions for economic mobility for the LMI populations they serve. Each respondent then had the opportunity to answer community conditions questions related to various topic areas depending on their organization’s involvement in those issues with LMI populations.

About the respondents

Do you work for an organization that provides services to low- to moderate-income households? If so, sign up External Linkhere to participate in future surveys. The survey is conducted twice each year and takes approximately 15 minutes to complete.