The COVID-19 pandemic has changed the way most consumers work and live. Shelter-in-place orders and fear of exposure to the virus have led businesses to expand their digital offerings and consumers to rely increasingly on mobile and online channels to conduct day-to-day activities. Increased digital activity has also meant a rise in the volume of digital payments. If these changes become the “new normal,” the pandemic may reshape the digital payments landscape in the longer term.

However, not all consumers have made the shift to digital payments. Some face financial or technological barriers that may require legislation or industry changes to address. In this Payments System Research Briefing, we examine why some consumers may not have adopted digital payments prior to the COVID-19 outbreak and how the pandemic is encouraging and enabling greater adoption. We also highlight legislative and industry initiatives that may facilitate consumer adoption of digital payments going forward.

Barriers to Adopting Digital Payments

As the world has become more digital, businesses have increasingly offered consumers online or mobile transaction options. But two fundamental barriers may keep consumers from adopting these digital options: the lack of a financial account for making or receiving payments (financial exclusion) and the lack of internet access at home (digital exclusion)._

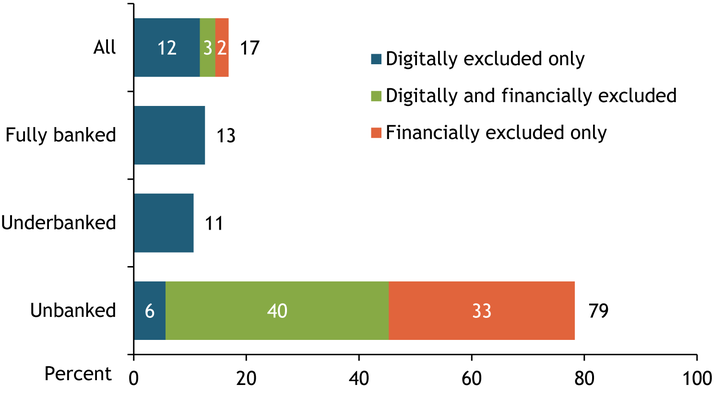

Chart 1 shows the shares of U.S. households that are financially or digitally excluded from digital payments, using data from the Federal Deposit Insurance Corporation’s 2017 Survey of Unbanked and Underbanked Households (FDIC survey). Prior to the coronavirus pandemic, around 17 percent of all households in the United States were financially or digitally excluded from using digital payments._ A vast majority of these households (12 percent) had a bank account or prepaid card but lacked internet access at home (blue bar). Of the remainder, 3 percent lacked internet access and a financial account (green bar), and 2 percent lacked an account but had internet access (orange bar).

Chart 1: Share of U.S. Households Financially or Digitally Excluded from Digital Payments by Banking Status, 2017

Sources: Federal Deposit Insurance Corporation and authors’ calculations.

Unbanked households were significantly more likely than fully banked and underbanked households to be excluded from digital payments, as they faced financial exclusion on top of digital exclusion (banked households by definition are financially included)._Financial exclusion was the more prevalent barrier among unbanked households by far—as of 2017, a vast majority (73 percent) of unbanked households did not own prepaid cards (green added to orange bars), while only 46 percent (blue added to green bars) did not have home internet access. However, unbanked households were also much more likely to face digital exclusion than their banked or underbanked counterparts.

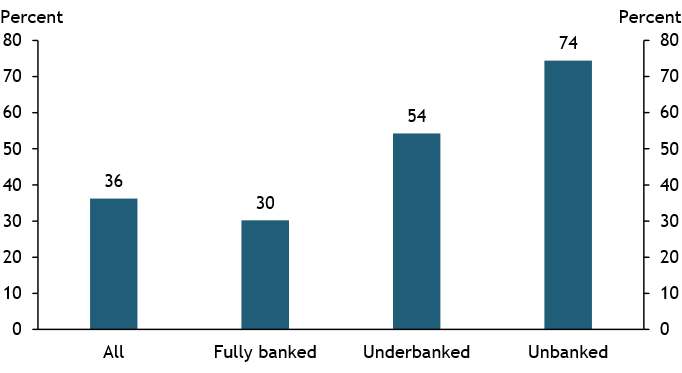

In addition to financial and digital exclusion, consumers may face less severe constraints to adopting digital payments. We can infer the presence of these constraints given that many financially and digitally included consumers have continued to use paper-based methods (cash, check, or money order) to pay bills and receive income. Chart 2 uses FDIC survey data on the prevalence of paper-based bill payment and income receipt methods to calculate the shares of digitally and financially included consumers that may have faced additional barriers to adopting digital payments. The first blue bar shows that prior to the pandemic, 36 percent of households that were financially and digitally included may have encountered difficulties paying bills or receiving income through digital channels._ The shares are much higher for underbanked (54 percent) and unbanked (74 percent) households than for their fully banked counterparts (30 percent).

Chart 2: Shares of Financially and Digitally Included Households that Faced Additional Digital Payment Constraints, 2017

Sources: Federal Deposit Insurance Corporation and authors’ calculations.

Some financially and digitally included consumers may not be able to use digital payment methods because the parties they transact with, such as billers and employers, do not offer or accept these payment methods. Some billers, particularly healthcare providers, may be deterred from offering digital payment options from fear of violating data privacy regulations, such as those imposed by the Health Insurance Portability and Accountability Act (Keesara, Jonas, and Shulman 2020). Others may only accept specific paper-based payment methods due to their lower transaction risks; for example, landlords often insist on rent payment via money order or cashier’s check because the underlying funds are guaranteed to be available. The higher share of renters among the financially underserved prior to the pandemic likely posed a barrier to their adoption of digital payments and contributed to their tendency to use paper-based methods.

In addition, consumers who work at small and mid-sized enterprises may not be offered the option to receive their paycheck digitally (such as through direct deposit)._ Smaller employers in particular may lack the internal resources to manage a digital payroll system or be deterred by the potential privacy risks of collecting employees’ bank account information (Deluxe 2020).

When digital options are available, cash flow constraints may keep some financially and digitally included consumers from using these methods to receive income. Even with direct deposits, funds from paychecks are typically not available instantly; automated clearinghouse (ACH) payments, for example, usually take one to two business days to arrive. Many consumers with cash flow constraints may therefore opt to receive income as cash so that they can access funds immediately.

Overall, we assess that approximately four in 10 households prior to the pandemic may have faced barriers or constraints to adopting digital payments. Notably, financially underserved (underbanked and unbanked) households, particularly unbanked households, were substantially more likely to encounter obstacles to using digital payments. Thus, at the onset of the COVID-19 pandemic, many financially underserved households were unlikely to be able to switch to digital payment methods._

How the COVID-19 Pandemic May Help Break Barriers to Digital Payments Adoption

Although legislators and the payments and telecommunications industries took steps before the pandemic to address barriers and constraints to adopting digital payments, progress has been slow, due at least in part to the high costs of investment in infrastructure, technologies, and training along with a lack of urgency. The COVID-19 pandemic may prove to be the needed catalyst for change. The pandemic has fostered a digital shift in the behaviors and preferences of consumers and businesses, spurred industry initiatives, and strengthened legislative efforts to address the prevailing gaps in consumer access to financial services and affordable broadband internet.

The digital shift in preferences and behaviors of consumers and businesses

The COVID-19 pandemic has led many consumers to increasingly use online and mobile channels to carry out their daily activities, including making and receiving payments. Consumers are shopping more online or through mobile apps and relying more on digital payment methods even for in-person transactions to avoid contact with cash or card readers (Kharif 2020). Many have also adopted mobile payment apps to send money to others. Zelle, a real-time mobile person-to-person (P2P) payment service provider, has seen substantial increases in both enrollment and use of its app since March 2020 (Zelle 2020).

Consumers’ desire to quickly receive the Coronavirus Aid, Relief, and Economic Security (CARES) Act’s Economic Impact Payments (EIP) may have further boosted digital payment adoption, particularly among the unbanked. Direct deposit should allow consumers to receive their EIP much sooner than through the mailing and processing of paper checks distributed at a later date, providing a strong incentive for eligible unbanked consumers to open bank, prepaid card, or transaction accounts. In April alone, the number of PayPal accounts increased by 7.4 million (135 percent growth), evidence that consumers may have opened new accounts in response to news about the EIP disbursement (Moeser 2020)._

The pandemic may also motivate businesses to accelerate the implementation of digital strategies. Many consumers and employees are concerned about potential exposure to COVID-19 when using contact-based payment methods. To address these concerns, more banks are beginning to deploy contactless cards, and some businesses have sped up their adoption of contactless POS terminals. Others have enabled customers to place and pay for their orders through mobile apps before picking them up (Kharif 2020). Meanwhile, shelter-in-place and social distancing mandates have compelled many businesses that were reluctant to make the digital transition pre-pandemic—notably, healthcare providers—to begin offering digital services and payment options (Gerdeman 2020).

Finally, increased worker demand for same-day pay arising from the pandemic may also lead more businesses—especially those that rely heavily on gig or ad hoc workers—to adopt same-day payroll solutions to assist or attract workers. For example, Domino’s Pizza recently partnered with Branch, a challenger bank, to offer its delivery drivers same-day wages, cash tips, and mileage reimbursements digitally (Adams 2020). Digital same-day pay options may make digital payments more feasible for cash-strapped consumers.

Payments industry initiatives

Many of the payments industry’s initiatives to help consumers navigate the COVID-19 crisis are also likely to facilitate digital payment adoption. Many banks and credit unions have waived certain service fees and charges, and some have also raised dollar limits associated with digital transactions—initiatives that may encourage their customers to retain their bank accounts and continue making digital payments. The initiatives of various nonbanks may also attract financially underserved consumers to open accounts with them, enabling these consumers to make and receive digital payments.

To provide relief to customers affected financially by the pandemic, several banks and credit unions are temporarily waiving transaction, service, or overdraft fees. Ally Bank, for example, has eliminated excessive transaction fees (for their savings and money account customers) and overdraft fees. It has also waived fees for the expedited shipping of debit cards. Similarly, BCU, an Illinois-based credit union, has waived overdraft and non-sufficient funds fees for members affected by the pandemic._These measures may enable those with low account balances to remain banked and continue making transactions digitally.

Some nonbanks have also made it easier and cheaper for unbanked and underbanked consumers to deposit checks through mobile apps. For example, PayPal enabled customers with a PayPal Cash Mastercard to receive their EIP directly into their PayPal account for free, while Netspend allowed customers to have their EIPs deposited directly via its mobile app and access the funds almost instantly on their Netspend prepaid debit cards. These initiatives may encourage underbanked and unbanked consumers to open accounts with these providers, which may, in turn, improve these consumers’ ability to conduct digital transactions.

Some payments industry players have also introduced new products or features to help businesses adapt to COVID-19 restrictions and respond to consumers’ increasing preference for digital or contactless payment methods. In late March, Square Inc. added two new features to its platform that enable businesses to provide curbside pickup or local delivery options at checkout. These features will likely shift some orders and payments from in-person to digital channels. More recently, PayPal launched a Quick-Response (QR) code app, which provides businesses with a simple and low-cost way to offer mobile payment options at the POS (Stewart 2020). To accept mobile payments, sellers only need to print out and display a QR code containing their payment information; customers scan this QR code using their PayPal app to pay._

Telecommunications industry initiatives

Telecommunications industry players have also introduced or participated in various initiatives to boost digital inclusion, particularly among consumers who lack or are at risk of losing internet access. Under the Federal Communications Commission’s (FCC) “Keep America Connected” initiative, over 750 telecommunications companies have pledged to maintain the internet access of households and small businesses that fall behind on their bills, to waive any late fees that these customers may incur, and to open their WiFi hotspots to any American in need through June 30, 2020 (FCC 2020).

Many participating internet service providers (ISPs) took their pledge to keep households connected even further. Some ISPs, such as AT&T, lifted data caps on their broadband internet plans, while others, including Charter Communications and Cable One, opened their WiFi hotspots to the general public. Several ISPs, including Atlantic Broadband and Comcast, are even offering consumers up to 60 days of complimentary broadband internet service (THE Journal 2020).

Partnerships between ISPs and state or local organizations have also emerged. Google Fiber partnered with DeKalb County Public Library in Decatur, Georgia, to launch the “Take the Internet Home with You” initiative, allowing patrons to borrow WiFi hotspots from the library for 21 days, even when the library was closed due to COVID-19 (Joplin 2020). Google Fiber has also partnered with United Way and the Community Services Community Investment Division of Orange County, California, to loan job seekers laptops and WiFi hotspots (Tsears 2020). Such initiatives are likely to allow more consumers to stay or become connected to the internet, in turn enabling them to make and receive digital payments—at least in the short term.

New and proposed legislation

The pandemic has brought financial and digital exclusion issues back to the forefront of policy debates with a greater urgency, leading to the introduction of several new laws and bills intended to close the gaps in financial and digital access. If implemented, many of these measures will likely improve the ability of financially or digitally underserved consumers to access digital payments.

To enable financially underserved consumers—particularly the unbanked—to receive COVID-19 relief payments more quickly and securely, the Bureau of Consumer Financial Protection recently issued a ruling that would allow for future COVID-19 relief payments to be disbursed through newly issued prepaid cards (Bureau of Consumer Financial Protection 2020). This ruling may pave the way for the broader disbursement of government benefits via prepaid cards, thereby increasing prepaid card ownership rates among unbanked consumers in the longer term. Consumers who have previously received other government benefits via paper checks may recognize the convenience of prepaid cards and opt to receive future government benefits on prepaid cards. An expansion of prepaid card ownership is likely to have a sizeable longer-term effect on unbanked consumers’ access to digital payments._

The pandemic has also spurred several states to sign up for a pilot program enabling Supplemental Nutrition Assistance Program (SNAP) recipients to use their SNAP benefits to purchase groceries online (PYMNTS 2020)._ Government regulations currently do not allow for the use of SNAP benefits for digital purchases, so SNAP recipients must do their grocery shopping in person even if they are worried about exposure to COVID-19. The pilot program may enable financially but not digitally excluded recipients to adopt digital payments, at least for their grocery purchases.

Some legislators have also proposed creating a digital dollar to distribute future COVID-19 relief payments. For example, the proposed Automatic Boost to Communities (ABC) Act calls on the Federal Reserve System to build and implement a system of Digital Dollar Account Wallets called “FedAccounts,” which would be accessible to all U.S. citizens, residents, and businesses. When coupled with digital inclusion, such a system could provide more consumers with access to digital payments and potentially increase financial inclusion.

The increased necessity of home internet access during the COVID-19 pandemic has also underscored the need for stronger legislative actions to bridge American’s “digital divide”—the wide disparities in consumers’ access to high-speed, or broadband, internet. Access to broadband internet at home may determine whether consumers can engage in telework, telemedicine, online learning, online shopping, and other activities digitally during the pandemic, as the availability of public WiFi may be limited. Many lower-income households and rural households lack such access due to the high cost or lack of availability of broadband internet services._ To bridge this digital divide, many lawmakers are calling for broadband infrastructure funding to be included in the next COVID-19 stimulus bill (McKinnon and Tracy 2020). If approved, this funding would help improve and expand the availability of broadband services, particularly in digitally underserved communities. As a result, more consumers may be able to adopt digital payments in the longer term.

Further Steps to Promote Digital Payment Adoption

While the initiatives discussed above may accelerate the adoption of digital payments, they do not fully address the underlying challenges many consumers face and may not result in widespread adoption. In particular, the initiatives introduced by the payments industry—especially banks and credit unions—may not adequately address consumers’ demand for quickly available funds when using traditional digital transaction methods. The delays associated with digital transaction methods such as ACH are likely the reason that up to 7 percent of households with the ability to make and receive digital payments opted to receive their income as cash before the pandemic._ Many of these households, particularly those with cash flow constraints, may continue to prefer receiving income via cash post-pandemic.

Widespread adoption of real-time payments—currently in the early stages of implementation in the United States—can help shorten delays in funds availability, thereby boosting consumers’ use of digital payments. Banks and credit unions play critical roles in enabling and promoting real-time payments adoption. These financial institutions not only connect their customers or members to the real-time payments infrastructure but also provide them with interfaces for conducting these transactions._ By developing user-friendly and convenient interfaces for making real-time payments, banks and credit unions may encourage more of their customers or members to adopt these payment methods.

As the COVID-19 pandemic continues, more consumers are likely to adopt digital payments. Aided by various legislative and industry initiatives, consumers and businesses are adapting to the new realities of the COVID-19 world by going digital. Whether this trend will continue post-pandemic remains to be seen—much will depend on whether the initiatives and momentum arising from this pandemic lead to sustained improvements in the ability of financially or digitally underserved consumers to participate in digital payments. Assisting unbanked and underbanked consumers in particular may require an array of stakeholders.

Endnotes

-

1

Although some consumers may have access to the internet outside their homes, lack of connection at home is still likely to limit their access to digital payments. The temporary closure of many workplaces and public spaces such as libraries due to the COVID-19 pandemic may further limit consumers’ access.

-

2

We consider households to have home internet access if they have broadband internet access or own a smartphone. Note that our proxy provides the upper bound of the share of households with internet access at home because not all smartphone owners have mobile data plans. Ideally, we would use the share of households with a mobile wireless internet account instead of smartphone ownership in our calculations, but the survey does not provide data on that share.

-

3

In the FDIC survey, unbanked households are households that do not have a bank account, underbanked households have a bank account but use alternative financial services (AFS), and fully banked households have a bank account and do not use AFS.

-

4

As a proxy for potential additional constraints to digital payments, we consider three uses of paper-based methods that we believe are more likely to be involuntary: paying bills by money order and receiving income via cash or check. Financially and digitally included consumers who used cash or checks for bill payment but did not conduct any other paper-based transactions are more likely to have used paper voluntarily. For instance, some of these consumers may have preferred paying with checks for in-person transactions prior to the pandemic but are likely able to switch to digital payments if necessary. We therefore do not consider these consumers to have faced additional constraints in our analysis.

-

5

Although receiving income via non-digital methods does not prevent consumers from transacting digitally, it introduces transaction frictions. To transact digitally, consumers must go through the hassle of first depositing the funds into their banks or prepaid card accounts. Moreover, when depositing paper checks, consumers may experience long delays before the funds are made available due to deposit holds.

-

6

Financially underserved consumers also have a higher tendency to face cash flow constraints. The pandemic is likely to worsen existing cash flow difficulties, further deterring these consumers from switching from cash to digital methods for income receipt.

-

7

PayPal Cash Plus Account holders could opt to receive their EIP via direct deposit into their account (PayPal 2020).

-

8

Smith and Foreman (2020) provide a list of banks and credit unions that are assisting their customers during the COVID-19 pandemic and the types of assistance they offer.

-

9

QR-code-based mobile payment methods have already been widely adopted in many parts of Asia (Bradford, Hayashi, and Toh 2019).

-

10

Based on the FDIC survey, 32 percent of unbanked households that own prepaid cards received them from the government.

-

11

States that have already launched digital SNAP payments include New York, Washington, Alabama, Iowa, Oregon, Nebraska, Florida, California, and Kentucky. The District of Columbia, Arizona, Idaho, North Carolina, West Virginia, Missouri, Texas, and Vermont have also recently signed up for the program but have yet to launch it (PYMNTS 2020).

-

12

Studies consistently find that lower-income households and rural households are substantially less likely to have access to broadband internet than their higher-income and urban counterparts. For examples, see Anderson (2018), Anderson and Kumar (2019), and Li and Sussman (2018).

-

13

Calculated based on data from the FDIC survey.

-

14

Hayashi and Toh (2020) discuss why mobile banking may be the best platform for consumers to access faster payments and highlight measures that may help increase the adoption of mobile banking services.

Article Citation

Zelle. 2020. “External LinkConsumers Leverage Zelle® to Send and Receive Money in Times of Need.” Press Release, April 27.

References

Adams, John. 2020. “External LinkGig Economy Payroll Players May Be Well Positioned for the Coronavirus Economy.” Payments Source, May 14.

Anderson, Monica. 2018. “External LinkAbout a Quarter of Rural Americans Say Access to High-Speed Internet Is a Major Problem.” Pew Research Center, Fact Tank, September 10.

Anderson, Monica, and Madhumitha Kumar. 2019. “Digital Divide Persists Even as Lower-Income Americans Make Gains in Tech Adoption.” Pew Research Center, Fact Tank, May 7.

Bradford, Terri, Fumiko Hayashi, and Ying Lei Toh. 2019. “Developments of QR Code-Based Mobile Payments in East Asia.” Federal Reserve Bank of Kansas City, Payments System Research Briefing, June.

Bureau of Consumer Financial Protection. 2020. “External LinkTreatment of Pandemic Relief Payments Under Regulation E and Application of the Compulsory Use Prohibition.” April 13.

Deluxe. 2020. “External LinkHow Businesses Can Give Gig Workers Much-Needed Digital Payment Options.” Deluxe, April 23.

Federal Communications Commission (FCC). 2020. “External LinkOver 750 Broadband and Telephone Providers Extend Keep Americans Connected Pledge.” Federal Communications Commission News, May 14.

Gerdeman, Julie. 2020. “External LinkContactless Patient Payments in the Era of COVID-19.” HealthPay24, CEO Spotlight, May 5.

Hayashi, Fumiko, and Ying Lei Toh. 2020. “External LinkMobile Banking Use and Consumer Readiness to Benefit from Faster Payments.” Federal Reserve Bank of Kansas City, Economic Review, forthcoming.

Joplin, Jill. 2020. “External LinkLibraries are helping bridge the digital divide during COVID-19.” Google Fiber, Community Impact, April 24.

Keesara, Sirina, Andrea Jonas, and Kevin Schulman. 2020. “External LinkCovid-19 and Health Care’s Digital Revolution.” New England Journal of Medicine, April 2.

Kharif, Olga. 2020. “External LinkContactless Payments Skyrocket Because No One Wants to Handle Cash.” Bloomberg, April 16.

Li, Austen, and Jacqueline Sussman. 2018. “External LinkBridging the Digital Divide.” Wharton University of Pennsylvania Public Policy Initiative, April 10.

McKinnon, John D., and Ryan Tracy. 2020. “External LinkPandemic Builds Momentum for Broadband Infrastructure Upgrade.” Dow Jones & Company, Wall Street Journal, April 23.

Moeser, Michael. 2020. “External LinkPayPal New Accounts Skyrocket — But Revenue Still Falls Short.” Payments Source, May 6.

PayPal. 2020. “External LinkReceive Your Government Stimulus Payment Directly Through PayPal.” April 11.

PYMNTS. 2020. “External LinkSNAP Users Shut Out of Digital Grocery Aisles.” May 4.

Smith, Kelly Anne, and Daphne Foreman. 2020. “External LinkList of Banks Offering Relief to Customers Affected by Coronavirus (COVID-19).” Forbes, May 3.

Stewart, John. 2020. “External LinkIn a Twist on Contactless, PayPal Rolls Out a QR Code App for Small and Occasional Sellers.” Digital Transactions, May 19.

THE Journal. 2020. “Updated: Free WiFi for Online Learning During COVID-19.” May 12.

Tsears. 2020. “External LinkCounty of Orange Teams Up with Google Fiber to Help Job Seekers Impacted by COVID-19.” Voice of OC, April 30.

Zelle. 2020. “External LinkConsumers Leverage Zelle® to Send and Receive Money in Times of Need.” Press Release, April 27.

Ying Lei Toh is an economist at the Federal Reserve Bank of Kansas City. Thao Tran is a research associate at the bank. The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.