The recent pandemic-induced downturn in the nation’s economy led to the largest quarterly decline in total income on record, as well as the largest recorded increase in unemployment. As businesses quickly adapted to serve their customers at a distance, incorporated remote work and took advantage of the Paycheck Protection Program to blunt the losses in employment and earnings, the share of total income retained by workers increased in 2020. Although the pandemic was an unprecedented shock, and the economic policies to counter the downturn were also unprecedented, the rise in the labor share of income during 2020 appears similar to past business cycles. In this edition of the Rocky Mountain Economist, we show that the outsized shifts in regional economic activity across sectors during the pandemic actually exacerbated the rise in labor’s share of income beyond what is typical during economic downturns. Even though job growth and wage growth have been strong over the past year, the recovery followed typical cyclical patterns with the labor share of income falling to previous norms by the end of 2021. Recent developments in global commodity markets, which directly affect the commodity-intensive economies of the Rocky Mountain region, are also likely to weigh further on the share of income going to workers. Still, the past year showed broad-based and robust growth in income for workers, business owners and capital owners.

Historical Ebbs and Flows in the Labor Share over the Business Cycle

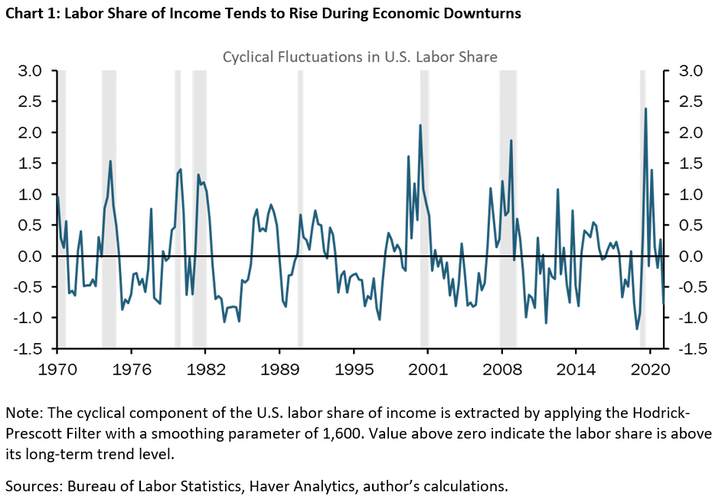

Over the past 50 years, labor’s share of income has moved counter to the rise and fall of overall economic activity. Labor income is typically measured as total wages and salaries earned by workers plus all proprietor income for small business owners, which includes gig workers and independent contractors. The labor share is simply total labor income as a share of gross domestic product (or gross state product), which is the total income generated by the U.S. economy (or state economies). Chart 1 shows the cyclical fluctuations in the U.S. labor share since 1970, with recession periods marked by gray bars. In each economic downturn, the labor share of income rose. This is not to suggest that employment and labor income rises during a cyclical downturn, but rather that other income, such as corporate earnings, tends to fall much faster than labor income during downturns, causing labor’s share to rise.

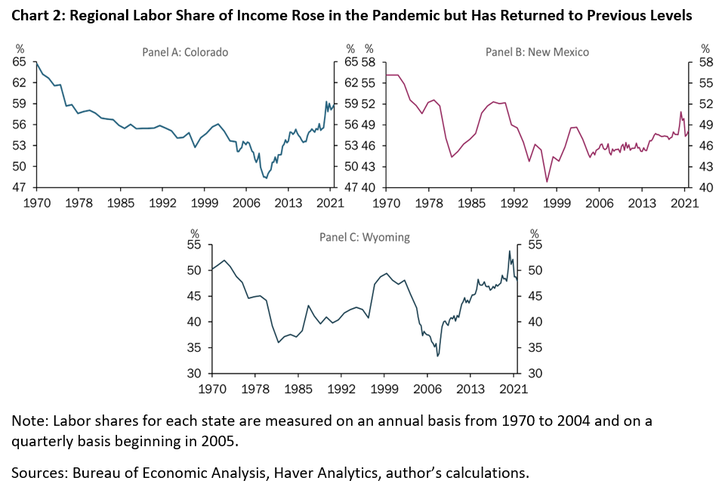

The economies of the Rocky Mountain region also experienced rising shares of income going to workers during 2020. Chart 2 shows between 2.5 and 5% more of total income was retained by workers in the region as overall economic activity fell sharply at the onset of the pandemic. The labor share rose in each state because wage and salary earners garnered a larger share of income. In contrast, the upward trend in the labor shares of Colorado and Wyoming after 2010 were attributable mostly to rising proprietor incomes of business owners and independent contractors. As the New Mexico and Wyoming economies recovered, the labor shares retraced their rise and returned to pre-pandemic norms by the end of 2021.

What Drove Labor’s Share of Income Up in 2020 and Back Down in 2021?

Profound shifts in economic activity across industries pushed labor shares higher in 2020, particularly in Wyoming and New Mexico. Movements in the overall labor share of income typically are driven by fluctuations within industries. That is to say, the total labor share rises during downturns because workers’ earnings within sectors – such as professional business services, oil and gas or information technology – decline by less than total industry activity declines. Likewise, during recoveries, total industry activity tends to recover faster than labor earnings grow, bringing the labor share of income back down to its trend level. Tüzemen, Marsh and Tran document the importance of movements within U.S. industries since the year 2000, while Elsby, Hobijn and Şahin show that changes in labor shares within industries have been the dominant factor for decades.

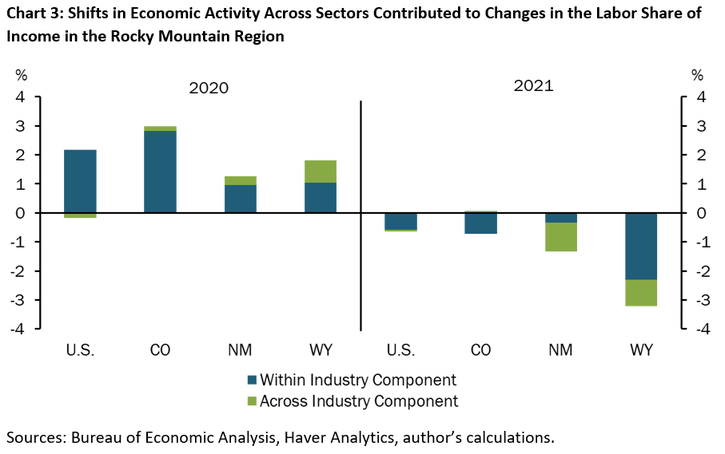

The pandemic was an atypical shock to economic activity that disproportionately affected specific industries. Unlike typical downturns, in 2020, regional activity shifted toward industries such as healthcare and social assistance, where the share of total industry income going to workers is relatively high, and away from oil and gas and transportation services, where the labor share is generally lower. This reallocation of activity across industries with different labor shares led to a larger increase in the total labor share of income during the first year of the pandemic, particularly in New Mexico and Wyoming. Of course, losses in employment and labor earning within industries were also profound. Chart 3 shows a simple shift-share analysis to separate the typical shifts in the labor share of income within industries (blue bars) and the atypical changes in the share of overall economic activity across industries (green bars).

A Look Ahead at the Labor Share of Income

On the heels of the economic recovery in 2021, this year began with a shock to global commodity markets that led to higher grain, energy and metals prices. Oil and gas sectors and other mining sectors are capital-intensive industries, having the lowest labor share of income compared with nearly all other sectors of the economy. As suggested by Manyika and co-authors, commodity booms that favor capital-intensive activities can act to suppress the labor share of income in the overall economy. In other words, the global economy is facing a commodity supercycle that has important implication for labor’s share of income in the region. Technological advancements in oil and gas extraction accelerated declines in labor usage in recent years, lowering the labor share within the industry even further. The surge in energy activity in Wyoming is a poignant example. Coal production and related activities increased with rising commodity prices in 2021, and so the energy and mining sectors became larger shares of the state economy. This shift in activity accounted for one-third of the decline Wyoming’s labor share last year, as shown in the green bars in Chart 3. As even more activity is directed to these capital-intensive industries amid higher commodity prices, the labor share of income is likely to further decline modestly.

_________________________

References

Elsby, Michael W.L., Bart Hobijn and Ayşgül Şahin. 2013. “The Decline in the U.S. Labor Share,” Brookings Papers on Economic Activity.

Manyika, James et al. 2019. “A New Look at the Declining Labor Share of Income in the United States,” McKinsey Global Institute Discussion Paper.

Tüzemen, Didem, Blake Marsh and Thao Tran. 2018. “Trends in the Labor Share Post-2000,” Economic Bulletin, Federal Reserve Bank of Kansas City.