Agricultural credit conditions in the Tenth District continued to deteriorate at a gradual pace in the third quarter. According to responses from the Survey of Agricultural Credit Conditions, farm income in the region was sharply lower, loan repayment was slightly slower and problem loan rates grew slightly. Loan demand increased as working capital declined and lenders reported an increase in asset liquidation. Despite the moderation in credit conditions and interest rates remaining at multi-decade highs, farm real estate values remained firm.

The outlook for the farm sector nearing the end of 2024 remained subdued alongside weak crop prices. Farm income and credit conditions continued to weaken more in areas most concentrated in crop production while the strength of cattle prices provided some support to other portions of the region. The considerable reduction in profits for crop producers has weakened farm balance sheets, increased demand for financing and could put further pressure on agricultural credit conditions in the months ahead.

Section 1: Farm Finances and Credit Conditions

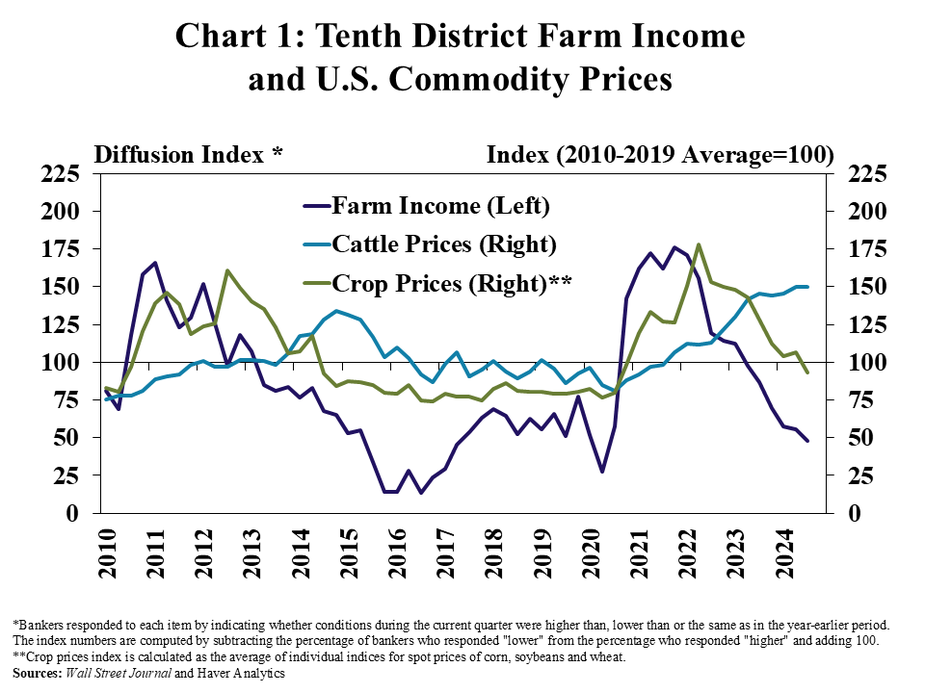

The pace of decline in farm income intensified as crop prices remained weak. About 60% of respondents reported that farm income was lower than a year ago and only 10% reported an increase, which was the lowest share since 2020 (Chart 1). Despite strong cattle prices, incomes in the region have contracted alongside sharply lower crop prices.

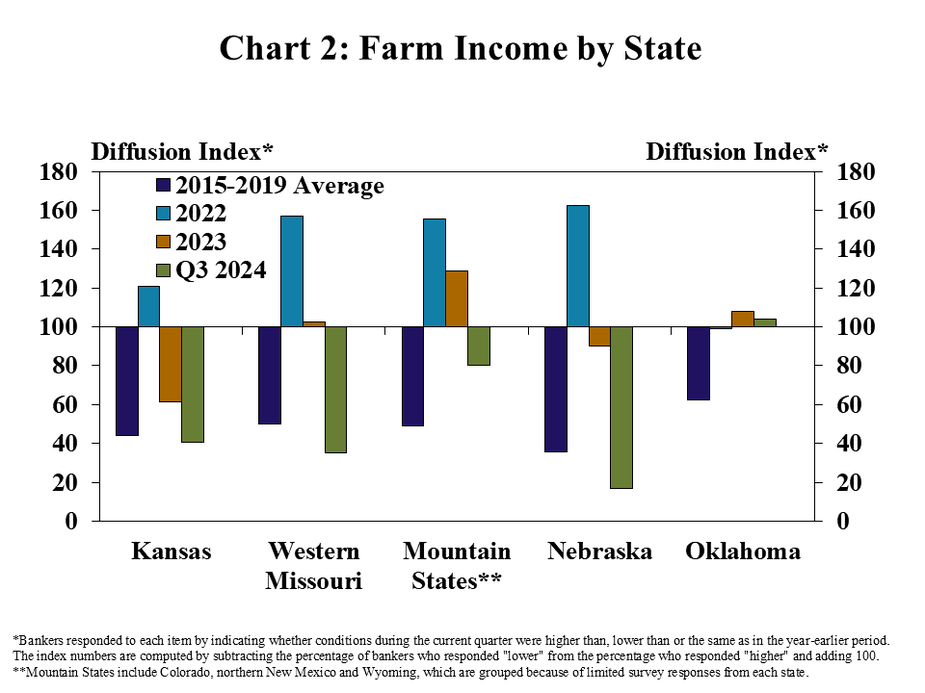

Farm incomes were comparably weaker in areas more concentrated in crop production. According to respondents, incomes weakened the most in Kansas, Missouri and Nebraska (Chart 2). In Oklahoma, conditions were largely stable, with 30% of lenders reporting incomes that were lower than a year ago and another 30% reporting that incomes were higher.

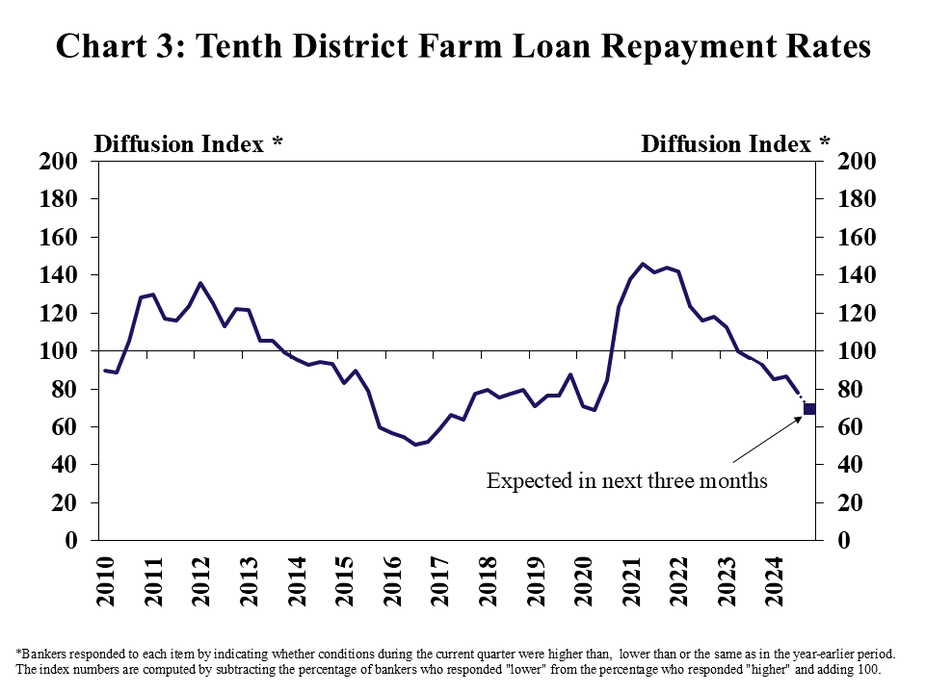

As farm finances softened further, the pace of decline in loan repayment rates picked up gradually. About 25% of respondents reported that farm loan repayment rates were lower than a year ago and less than 5% reported an increase (Chart 3). Looking ahead to the next three months, nearly 40% expected rates of repayment to decline.

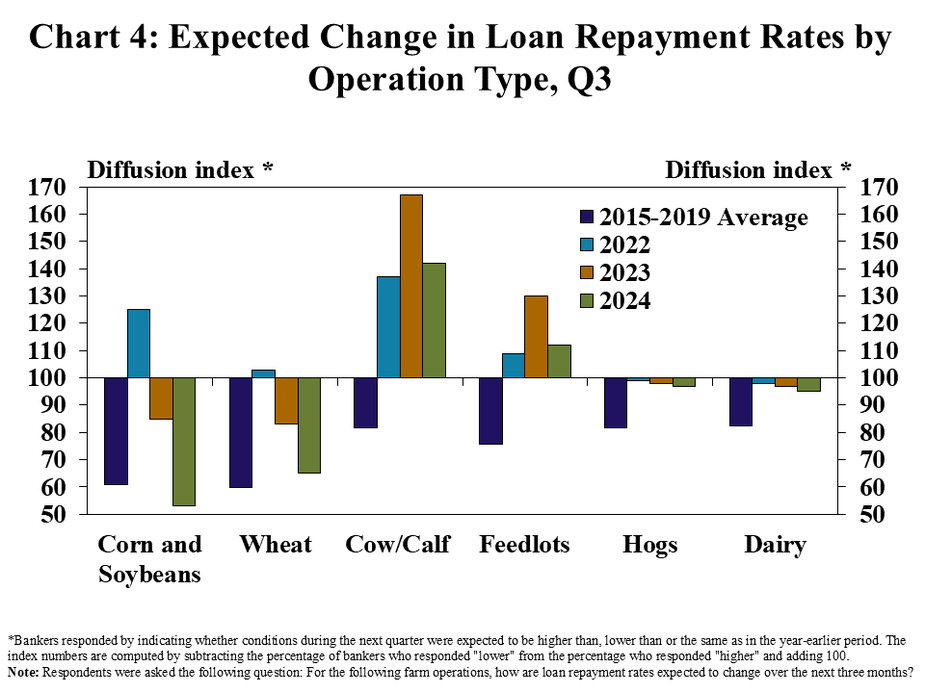

Deterioration in repayment was expected to be particularly notable for crop operations in the coming months. Respondents anticipated a considerable deterioration in repayment rates for corn, soybean and wheat producers but expected conditions for ranchers and feedlots to improve (Chart 4). For lenders with hog and dairy customers, loan repayment was expected to decline slightly in the coming months.

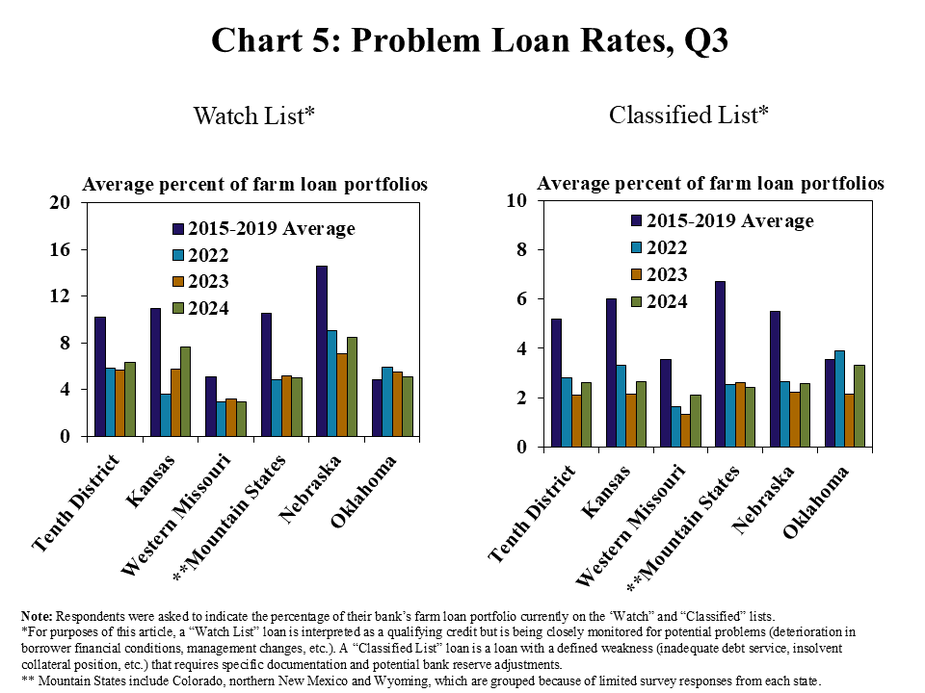

Alongside tighter repayment capacity, loan quality weakened slightly across the region. On average, about 6% and 3% of responding banks’ loan portfolios were on the watch and classified lists, respectively (Chart 5). Lenders in nearly all states reported a slight increase in problem loan rates following historically strong loan quality in recent years.

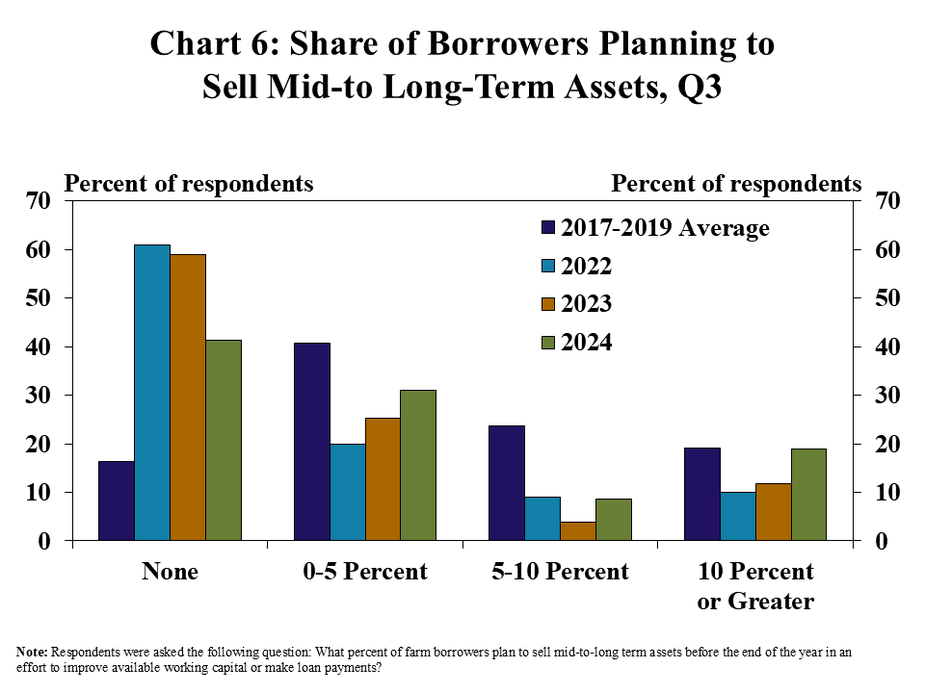

Asset liquidation also increased notably from recent years. About 60% of responding banks reported that at least a fraction of farm borrowers planned to sell assets in the coming months to improve working capital or make loan payments (Chart 6). About a fifth of respondents reported that more than 10% of borrowers had liquidation plans.

Section 2: Interest Rates, Lending Activity and Farmland Values

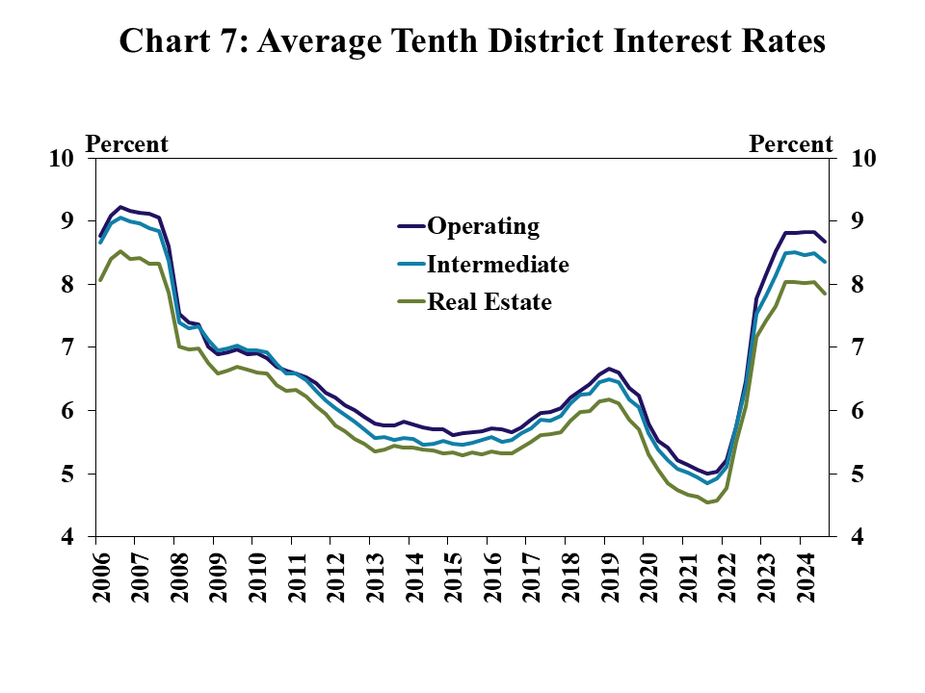

Interest rates on farm loans inched lower alongside recent cuts in benchmark interest rates. Lenders reported a modest 15 basis point decrease in average interest rates for ag loans, following two quarters of virtually no change (Chart 7). The spread between rates on operating loans and farm real estate reached 81 basis point, about twice as high as the average observed after 2010.

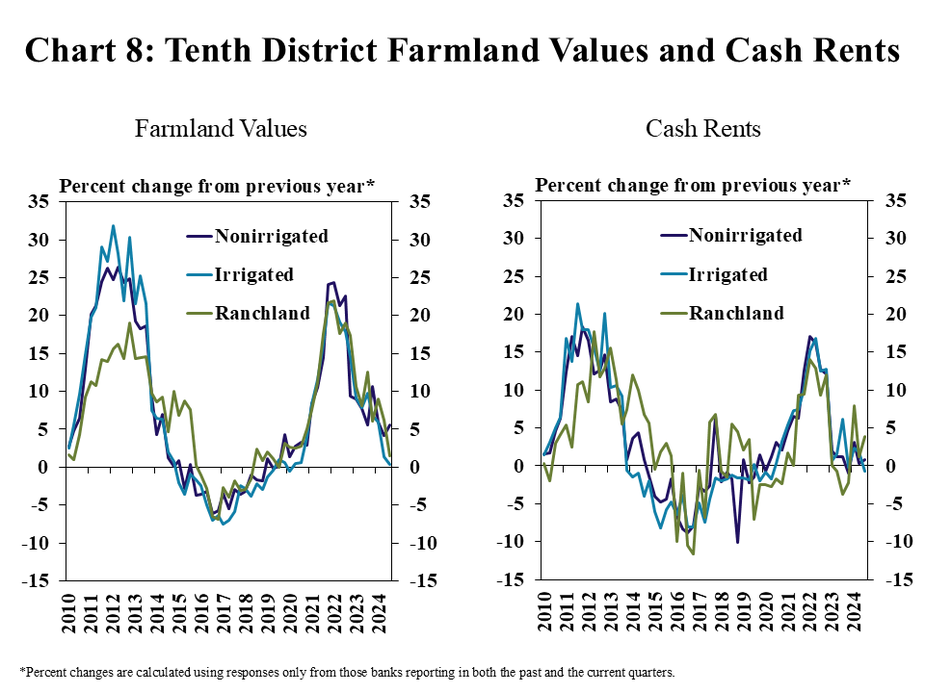

Despite fewer opportunities for profits in the crop sector, agricultural real estate values held firm. The value of nonirrigated cropland was 5% higher than one year ago in the third quarter (chart 8). Irrigated cropland and ranchland values also increased from a year ago but at a more modest pace of 0.3% and 1.6%, respectively. Cash rents on irrigated and nonirrigated cropland were nearly unchanged from a year ago, while rents on ranchland increased about 4% and have been more volatile in recent periods.

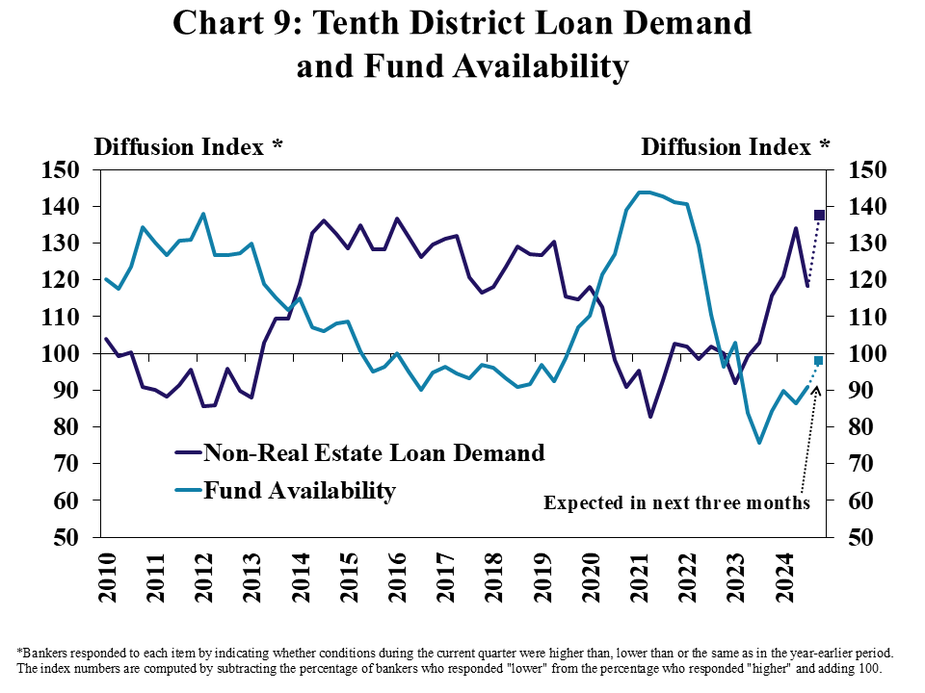

Farm loan demand remained high, while fund availability continued to moderate. A higher share of lenders reported an increase in demand for non-real estate ag loans from a year ago, and an even higher share expected growth in demand for loans in the coming months (Chart 9). While more respondents reported a decline than an increase in fund availability, expectations for the coming months were more balanced.

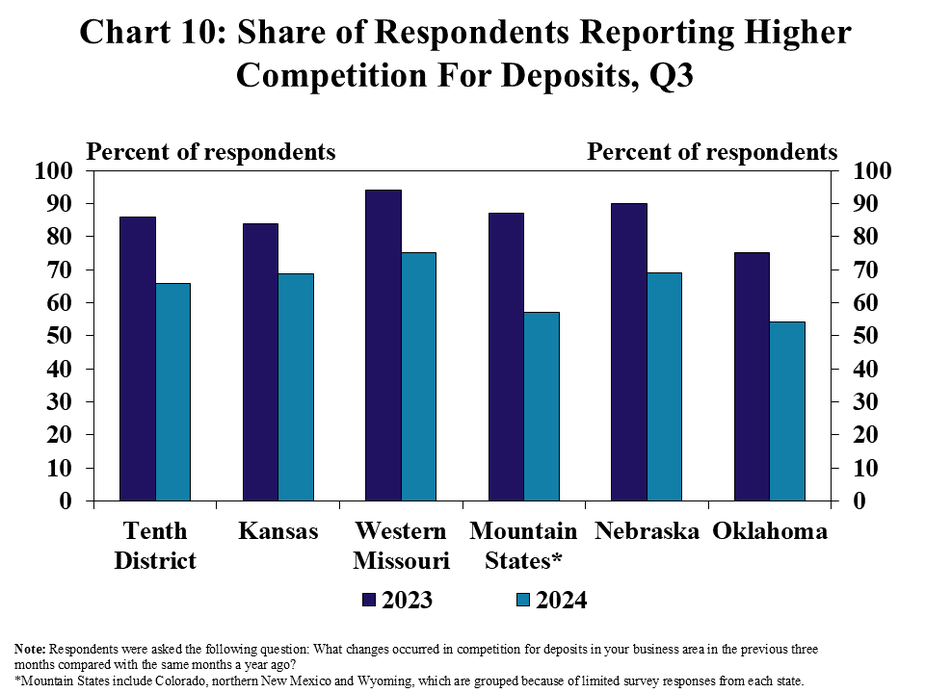

Competition for deposits also remained high but less fierce than a year ago. More than 60% of respondents reported higher competition for deposits this year, down from the more than 80% in 2023 (Chart 10). Almost 75% of banks in Western Missouri indicated stronger competition for deposits, the highest among the states in the region, while a little more than half of contacts in the Mountain States and Oklahoma indicated more competition for deposits.

Banker Comments Q4 2023

“Input cost are too high to make the low grain prices profitable and dry weather has significantly impacted the ranchers and farmers also.”– Colorado

“Current grain prices are putting continued pressure on margins and most farmers have recognized the lack of profitability and have pulled back spending.” – Kansas

“Low commodity prices have driven demand for short term assets down, especially when combined with high interest rates. But we are seeing customers with good size cattle herds doing well.”– Kansas

“Lower crop prices & increased family living expense have put pressure on farming operations.”– Kansas

“Low commodity prices have producers concerned about zeroing their lines of credit. Some are seeking off-farm jobs to assist with higher insurance costs and living expenses and cash reserves are running on fumes for farmers and non-farmers.”– Missouri

“Inflation continues to impact farmers, businesses and consumers in our area.”– Missouri

“High calf prices are having a positive impact on cow/calf operations but are limiting the numbers of local feedlots willing to purchase the cattle to put on feed.”– Nebraska

“Summer farm inspections almost all indicated deterioration of working capital with almost no exceptions.”– Nebraska

“Lower prices for corn and soybeans will hurt farm incomes, however, harvest is underway with very good yields to help offset lower prices.”– Nebraska

“Cashflow and repayment are expected to be down due to the price of corn.”– Oklahoma

“If interest rates begin to go down, it should alleviate this stress borrowers had from the rapid increase we had.”– Oklahoma

A total of 135 banks responded to the Third Quarter Survey of Agricultural Credit Conditions in the Tenth Federal Reserve District—an area that includes Colorado, Kansas, Nebraska, Oklahoma, Wyoming, the northern half of New Mexico and the western third of Missouri. Please refer questions to Francisco Scott, economist or Ty Kreitman, associate economist at 1-800-333-1040.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.