Agricultural real estate values in the Kansas City Federal Reserve District were flat through the end of 2024 and credit conditions deteriorated slightly. According to lenders in the region, the value of nonirrigated farmland changed by less than 1% compared with the previous year. Land market conditions varied in some states, but in aggregate, values were generally unchanged, and sales volumes slowed over the past year as the farm economy weakened and farm loan interest rates remained at multi-decade highs. Alongside subdued economic conditions, the share of lenders reporting lower farm income and loan repayment rates increased into the fourth quarter and demand for non-real estate financing grew.

Economic conditions in agriculture were subdued through the end of 2024 alongside weak crop prices. In early February, the United States Department of Agriculture (USDA) forecasted considerable improvement in net farm income in 2025 alongside substantial ad hoc government payments associated with the American Relief Act of 2025. The outlook for crop revenues remained weak, but distribution of recently announced payments for disaster relief and economic assistance in the coming months could support farm finances in the year ahead.

Tenth District Farmland Markets

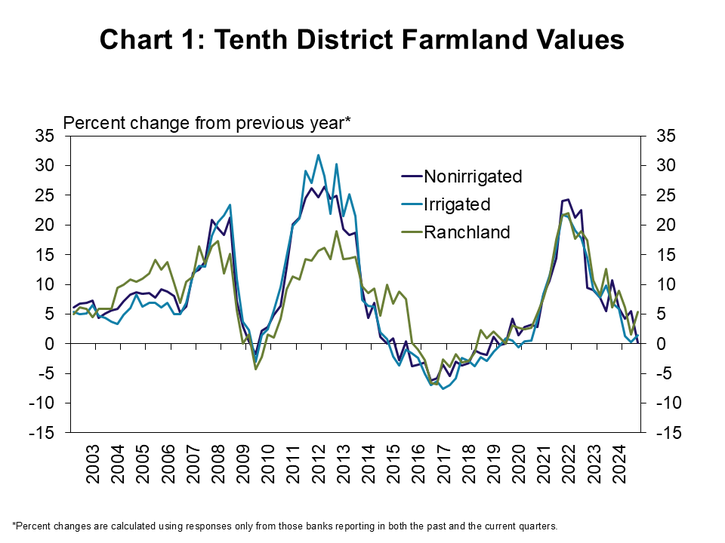

Growth in farm real estate values in the Tenth Federal Reserve District flattened in 2024. According to survey respondents, the value of nonirrigated and irrigated farmland in the region increased less than 1% and about 2% from the prior year, respectively (Chart 1). Ranchland values grew slightly more during the final months of the year and increased by an average of about 5% over the past four quarters.

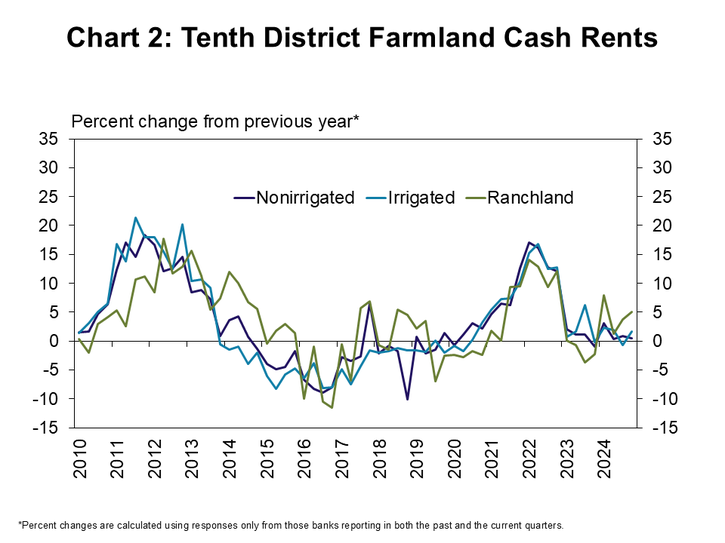

Cash rents for farmland also generally remained unchanged throughout the past year. Similar to land values, rental rates charged on farmland in the District increased by less than 2% (Chart 2). Also following a similar path, ranchland cash rents increased by about 5% from the previous year.

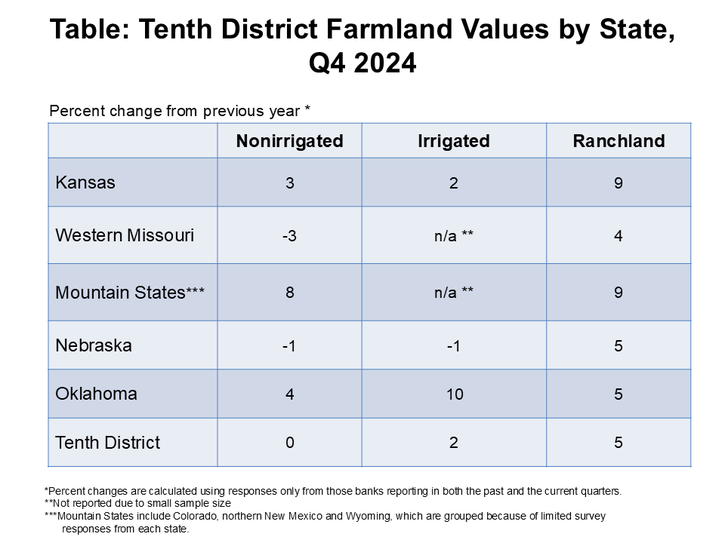

Changes in values varied across states and types of land. The value of nonirrigated land declined slightly in western Missouri and Nebraska but increased modestly in other states (Table). Ranchland values grew at least modestly in all states with slightly stronger growth in Kansas and the Mountain States.

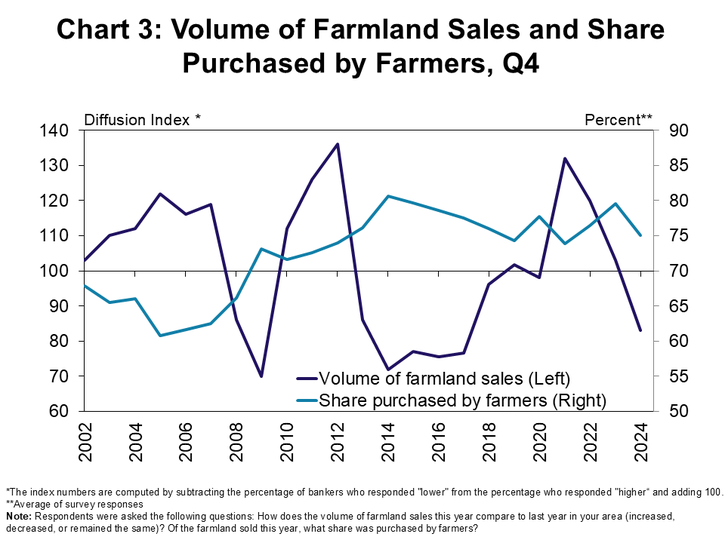

Farmland markets cooled alongside lower sale volumes and steady demand from farmers. The volume of farmland sales in the region was less than a year ago according to lenders (Chart 3). Similar to recent years, respondents on average reported that about 75% of all land purchases were made by farmers.

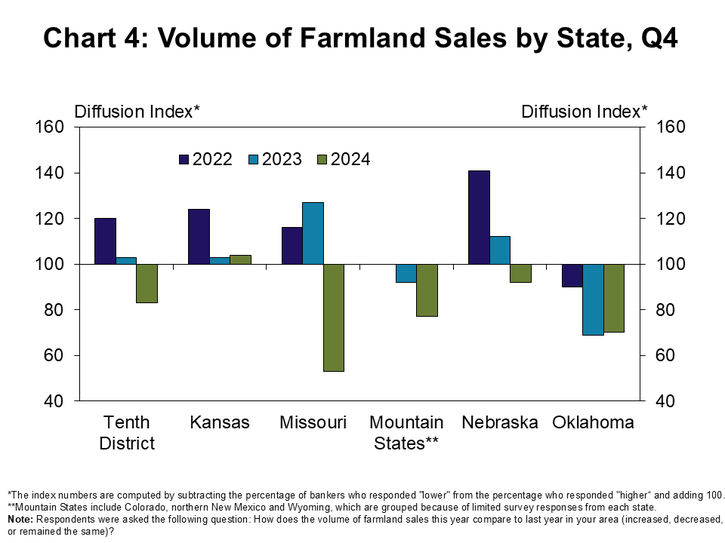

The slowdown in sales was most pronounced in Missouri and Oklahoma. About 50% of lenders in Missouri and Oklahoma reported that sales volumes in the fourth quarter were down from a year earlier (Chart 4). In other states, only about 30% reported lower sales and in Kansas the share was less than 15%.

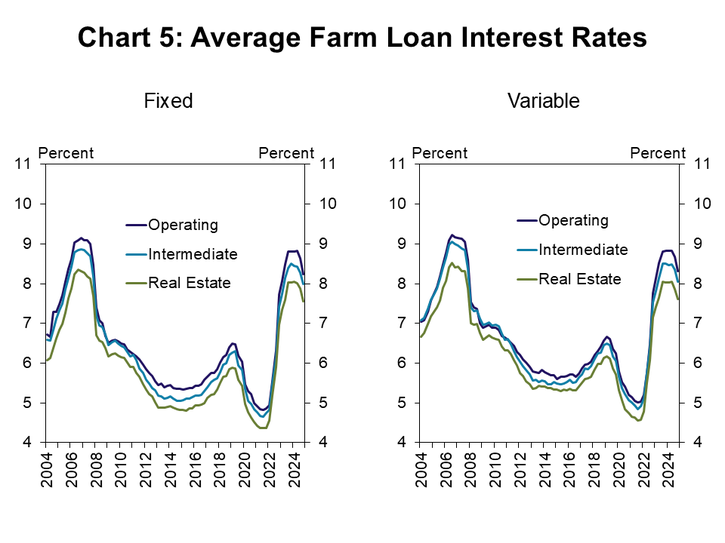

Activity in land markets slowed as agricultural economic conditions weakened and farm loan interest rates remained at multi-decade highs. Fixed and variable rates on all types of agricultural loans declined about 30 basis points from the previous quarter and were around 50 basis points less than the beginning of 2024 (Chart 5). Rates fell alongside lower benchmark rates, but remained above the average over the past 20 years.

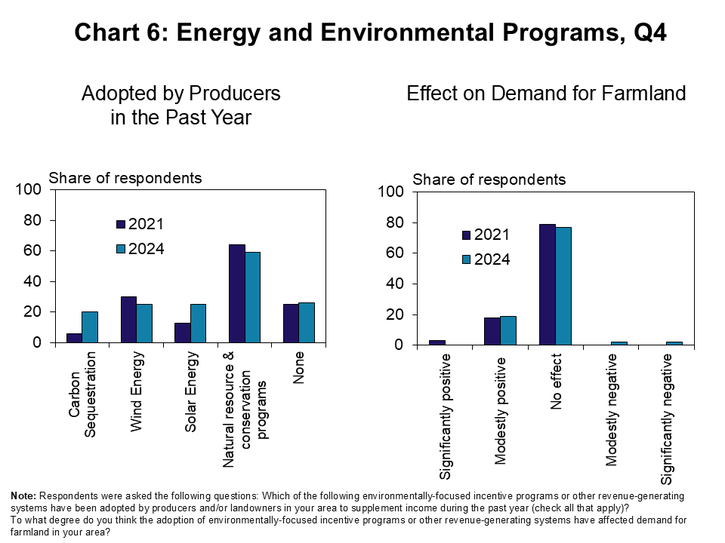

Adoption of emerging energy-related activities had a limited effect on demand for farmland. According to lenders, implementation of carbon sequestration practices and solar energy by landowners was more pronounced than a few years ago (Chart 6, left panel). Despite more adoption of these types of practices, lenders indicated that the impact on demand for farmland has been modest (Chart 6, right panel).

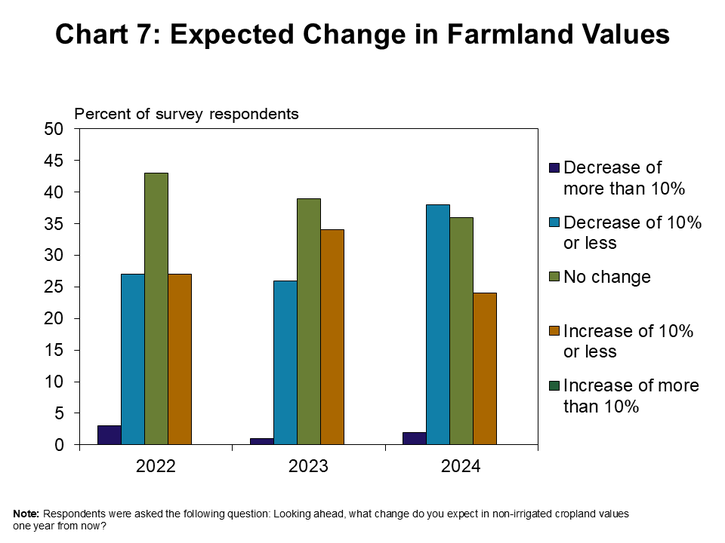

A growing share of lenders expect slight deterioration in land values over the next year. About 40% of respondents anticipated a modest drop in farmland values in 2025, a slightly higher share than last year (Chart 7). Another third expected no change in values while a smaller portion thought a modest increase was in the outlook.

Credit Conditions and Interest Rates

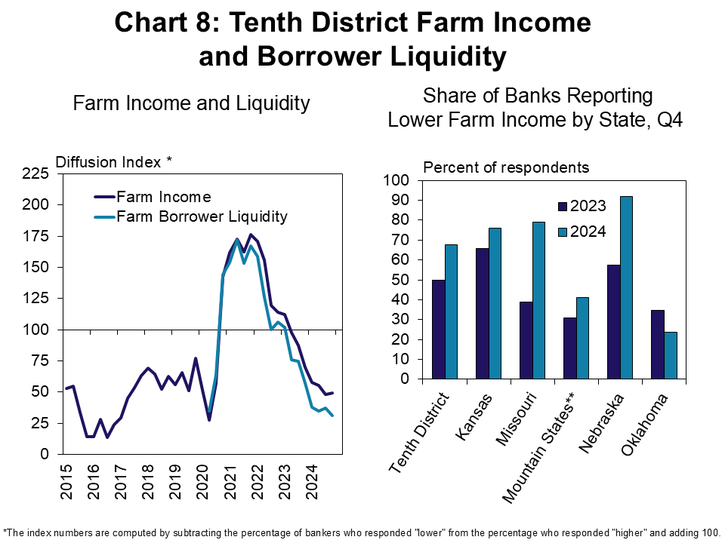

The more pessimistic outlook for agricultural land values coincided with tightening in farm financial conditions throughout the year. Farm income and liquidity in the region continued to decline at a sharp pace (Chart 8). Compared with the fourth quarter of 2023, the share of lenders reporting that income and liquidity were lower than the same time a year ago increased in all states expect Oklahoma.

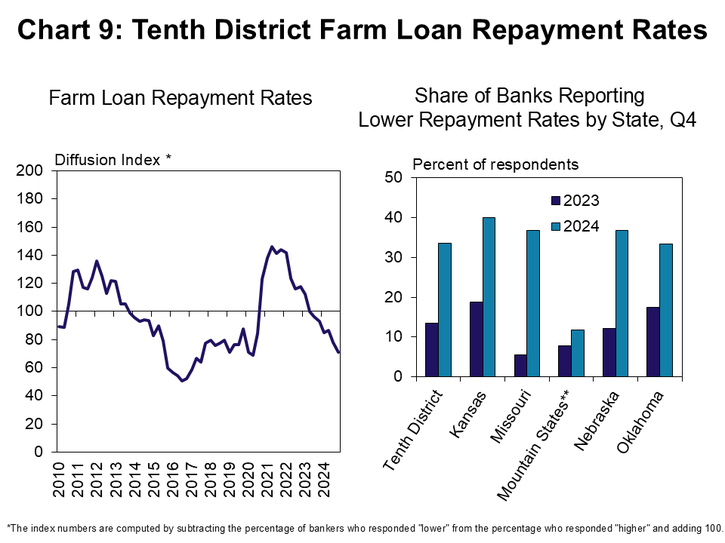

With lower farm income and liquidity, credit conditions deteriorated steadily. Farm loan repayment rates in the region declined at the fastest pace since early 2020 (Chart 9). The share of lenders indicating that repayment rates were lower than a year ago grew in all states over the past year.

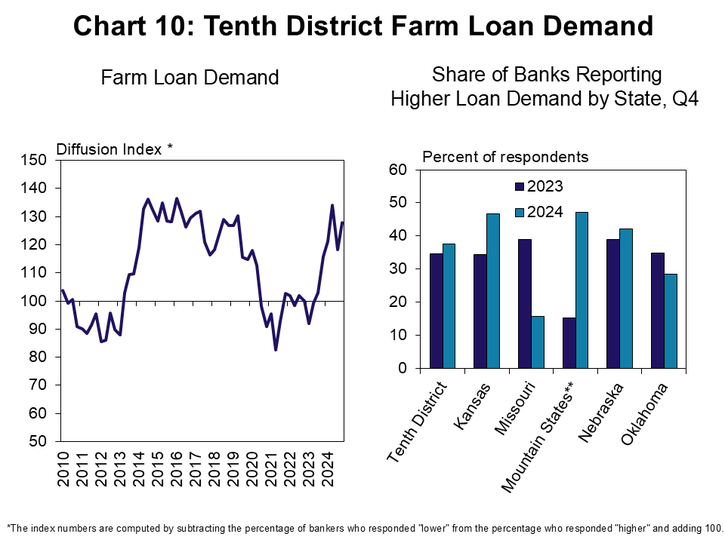

The reduction in cash on farmer balance sheets also contributed to growing demand for financing. Demand for non-real estate farm loans continued to increase at a moderate pace across the region (Chart 10). The share of lenders reporting higher loan demand grew considerably in the Mountain States, but dropped notably in Missouri.

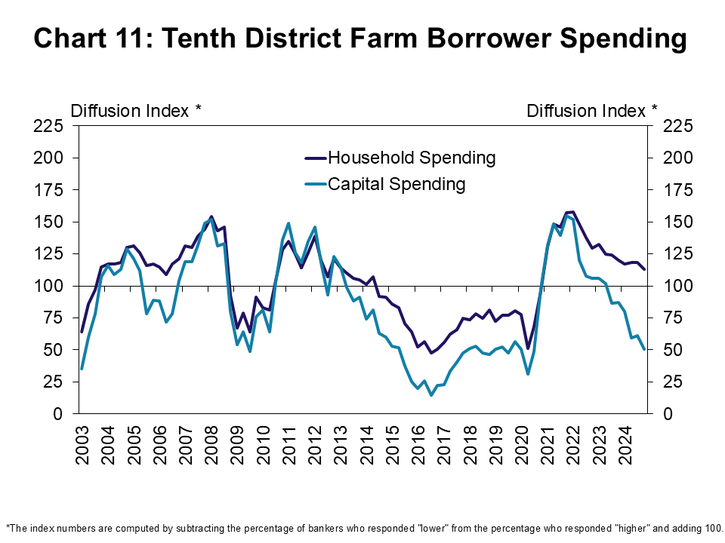

Farm borrowers cut back on capital spending in response to tighter finances, but pressure on household budgets persisted. Similar to the trend over the past year, the pace of decline in capital spending grew steadily while household spending continued to increase modestly (Chart 11). Producers have appeared to quickly reduce spending on equipment and other investments alongside lower incomes, but broad inflationary pressures have likely limited the capacity to cut household expenses.

Banker Comments Q4 2024

“Prolonged drought in some areas has affected borrower liquidity. Cattle producers are sitting well while row crop heavy farmers are struggling with low grain prices.”– Kansas

“Continued pressure on grain prices will impact local farmers.”– Missouri

“Operating lines are upside down and going backwards for three years in a row due to extreme drought paired with low commodity prices.”– Kansas

“Poor commodity prices are negatively impacting liquidity and repayment ability.”– Nebraska

“The just passed [ad hoc assistance] will help improve cash flows, but most all crop producers will still be close or below a breakeven.” – Oklahoma

“Cattle producers typically saw a good year with higher farm income and balance sheet liquidity when compared to row crop farmers.”– Nebraska

“Wind and Solar energy generation has had limited impact to most of our area.” – Kansas

“The demand for property for wind and solar energy use could increase demand for farmland depending on location.” – Oklahoma

“[Top of mind issues in our area are] increased cost of insurance and availability of water for irrigation as the Kansas aquifer levels are seriously depleted.” – Nebraska

“[Poor crop growing conditions] and lower crop prices made per acre income a lot less than the farmers had hoped for, and this is causing liquidity issues when making loan payments and paying off operating loans.” - Kansas

A total of 125 banks responded to the Fourth Quarter Survey of Agricultural Credit Conditions in the Tenth Federal Reserve District—an area that includes Colorado, Kansas, Nebraska, Oklahoma, Wyoming, the northern half of New Mexico and the western third of Missouri. Please refer questions to Nathan Kauffman, Senior Vice President and Omaha Branch Executive or Ty Kreitman, associate economist at 1-800-333-1040.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.