Since mid-2018, the manufacturing sector has been in a decline. After reaching a near-term high in August 2018, the Institute for Supply Management's (ISM) manufacturing index has steadily fallen to a level below 50, indicating contraction in this sector. Over the same period, job growth in the manufacturing sector fell from about 20,000 jobs per month to essentially none. These declines may have broad implications for states with a greater share of manufacturing activity and employment. For example, if the decline in manufacturing activity leads to reductions in hours worked, layoffs, or heightened uncertainty, consumers may pull back on purchasing goods and services.

The 2014–15 downturn in manufacturing may provide some clues as to how the current downturn will be resolved. Indeed, much like in the current downturn, manufacturing activity and employment decelerated markedly in the initial stages of the 2014–15 downturn. However, to the extent that each downturn was caused by different economic shocks, the response of consumption may differ.

We investigate whether the importance of manufacturing to a state’s economy is related to changes in state-level consumption growth during each of the two downturns._ We proxy for the importance of manufacturing using the share of workers employed in manufacturing in each state and calculate the shares in 2005 to keep our measure from being affected by the shocks that caused these downturns._

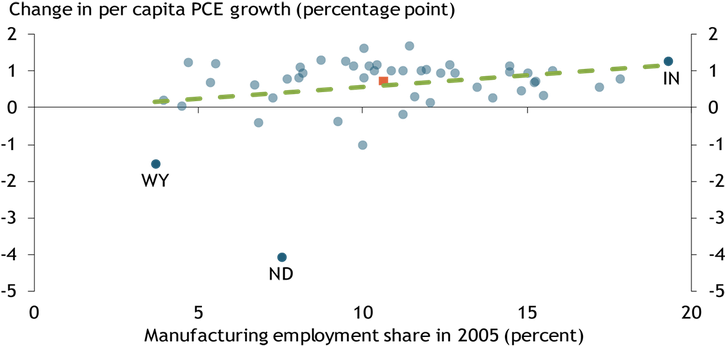

Chart 1 shows that during the 2014–15 downturn, consumption growth increased in states with a higher share of workers employed in manufacturing (hereafter, “manufacturing-heavy states”). The blue dots in Chart 1 represent the 48 contiguous states in our sample, while the dashed green line shows the line of best fit for the data. The positive slope of the green line suggests manufacturing-heavy states also had larger positive changes in consumption growth. For example, in Indiana, the state with the highest manufacturing employment share (19 percent), consumption growth increased by 1.3 percentage points, nearly double the increase for the United States as a whole (orange square). In contrast, in Wyoming and North Dakota, states with lower manufacturing shares (4 percent and 7.5 percent, respectively), consumption growth declined sharply. Consumption growth in Wyoming declined by roughly 1.5 percentage points from 2014 to 2015, while consumption growth in North Dakota fell by 4 percentage points.

Chart 1: State Consumption Growth in 2014–15 Relative to Manufacturing Importance

Notes: The orange square indicates the change for the United States as a whole. The line of best fit has a slope of 0.06, which is significant at the 10 percent level.

Sources: Bureau of Economic Analysis (Haver Analytics), Bureau of Labor Statistics (Haver Analytics), and authors’ calculations.

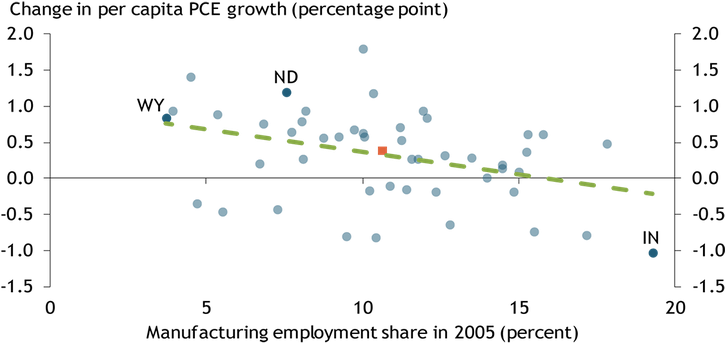

This pattern appears to have reversed during the 2018 downturn, as the correlation between a state’s share of workers in manufacturing and changes in consumption growth turned negative. Chart 2 shows that consumption growth in Indiana fell by 1 percentage point from 2017 to 2018, a time when consumption growth in the United States as a whole accelerated by nearly 0.5 percentage point (orange square). Over the same period, consumption growth increased by 0.8 percentage point in Wyoming and by 1.2 percentage points in North Dakota.

Chart 2: State Consumption Growth in 2017–18 Relative to Manufacturing Importance

Notes: The orange square indicates the change for the United States as a whole. The line of best fit has a slope of −0.06, which is significant at the 1 percent level.

Sources: Bureau of Economic Analysis (Haver Analytics), Bureau of Labor Statistics (Haver Analytics), and authors’ calculations.

Together, the results in Charts 1 and 2 suggest the relationship between manufacturing importance and consumption growth has changed since the 2014–15 downturn. This change is likely due to the different economic forces driving the two downturns. The 2014–15 downturn was due largely to a sharp decline in oil prices, which lowered gasoline prices and thereby boosted consumption growth in most states (including manufacturing-heavy states). The negative effects of the oil-price decline were largely concentrated in energy-producing states, such as Wyoming and North Dakota. Not surprisingly, both states saw their consumption growth fall during this period.

In contrast, oil prices have risen steadily throughout the 2018 downturn, leaving consumers with less money for other purchases. In addition, recent trade tensions may be discouraging consumption, particularly in manufacturing-heavy regions with a greater share of export activity. For example, Waugh (2019) finds growth in automobile sales from 2017 to 2019 was lower in counties more exposed to Chinese retaliatory tariffs. Consistent with this finding, changes in states’ durable goods consumption growth appear to be the main driver of the negative relationship seen in Chart 2._ More broadly, Amiti, Redding, and Weinstein (2019) estimate that tariffs caused U.S. real income to fall by roughly $1.4 billion per month in 2018, a substantial reduction that has likely weighed on consumption growth.

Overall, our results suggest that unlike the 2014–15 episode, consumers are responding to the weakness in manufacturing by pulling back on purchases. While this response is currently concentrated in manufacturing-heavy states, it could spill over into other states and sectors if trade tensions persist and demand continues to soften. Indeed, our results may understate the full response of consumption growth, as we only include data through 2018. The decline in manufacturing has since intensified, and the ISM index has recently moved into contractionary territory.

Endnotes

-

1

To calculate consumption growth, we use per capita consumption by state from the National Income and Product Account tables deflated by the overall personal consumption expenditures (PCE) chained price index indexed to 2012. While the Bureau of Economic Analysis provides implicit state-specific deflators, the 2018 data have yet to be released. Data on manufacturing employment shares are from the Bureau of Labor Statistics’ Establishment Survey.

-

2

Measuring the change in consumption growth helps us identify shifts in the behavior of consumption distinct from their typical patterns. For example, if states with a high share of workers employed in manufacturing tend to always have higher consumption growth than states with a low share of workers in manufacturing, looking at changes in consumption growth will net out this tendency. Our results do not change if we instead measure the change in consumption growth as a fraction of the state’s average consumption growth rate (measured over the entire 1997–2018 period for which we have data).

-

3

The correlation between manufacturing employment share in 2005 and change in durables consumption growth 2017–18 for the 48 contiguous states was −0.33. The line of best fit has a slope of −0.09, which is significant at the 5 percent level.

References

Amiti, Mary, Stephen J. Redding, and David Weinstein. 2019. “External LinkThe Impact of the 2018 Trade War on U.S. Prices and Welfare.” National Bureau of Economic Research, working paper no. 25672, March.

Waugh, Michael E. 2019. “External LinkThe Consumption Response to Trade Shocks: Evidence from the U.S.-China Trade War.” National Bureau of Economic Research, working paper no. 26353, October.

José Mustre-del-Río is a senior economist at the Federal Reserve Bank of Kansas City. Emily Pollard is an assistant economist at the bank. The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.