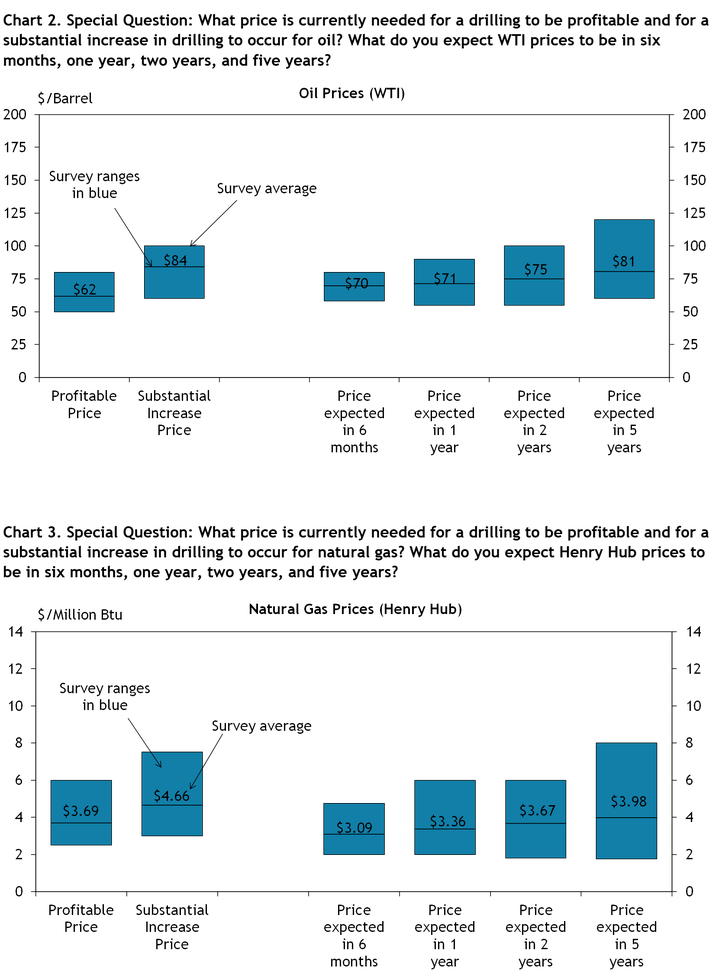

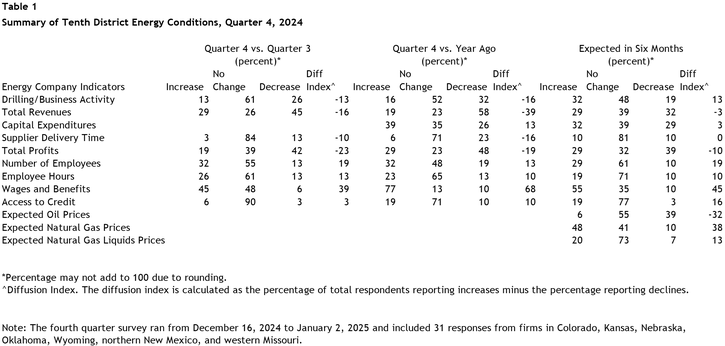

Fourth quarter energy survey results revealed that Tenth District energy activity fell at a steady pace while expectations rose. Firms reported that oil prices needed to be on average $62 per barrel for drilling to be profitable, and $84 per barrel for a substantial increase in drilling to occur. Natural gas prices needed to be $3.69 per million Btu for drilling to be profitable on average, and $4.66 per million Btu for drilling to increase substantially.

Summary of Quarterly Indicators

Tenth District energy activity declined further in the fourth quarter of 2024, as indicated by firms contacted between December 16th, 2024, and January 2nd, 2025 (Tables 1 & 2). The quarter-over-quarter drilling and business activity index was -13 in Q4, unchanged from the previous quarter (Chart 1). Employment and employee hours continued to increase even as revenues and profits declined further, falling to -16 and -23, respectively.

Drilling activity also remained down from this time last year, with the year-over-year drilling and business activity index at -16. Annual revenues decreased substantially at a reading of -39. However, employment and capital expenditures grew moderately, each posting readings of 13.

Firms anticipate a rebound in activity in the next six months, with the drilling expectations index rising from -3 in Q3 to 13 in Q4. However, revenues and profits are still expected to decline further in the coming months.

Chart 1. Drilling/Business Activity Indexes

Skip to data visualization table| Quarter | Vs. a Quarter Ago | Vs. a Year Ago |

|---|---|---|

| Q3 20 | 4 | -71 |

| Q4 20 | 40 | -60 |

| Q1 21 | 35 | 12 |

| Q2 21 | 33 | 59 |

| Q3 21 | 43 | 68 |

| Q4 21 | 32 | 74 |

| Q1 22 | 29 | 52 |

| Q2 22 | 57 | 77 |

| Q3 22 | 44 | 78 |

| Q4 22 | 6 | 56 |

| Q1 23 | -13 | 17 |

| Q2 23 | -19 | -16 |

| Q3 23 | -13 | -23 |

| Q4 23 | -33 | -33 |

| Q1 24 | -13 | -26 |

| Q2 24 | -14 | -25 |

| Q3 24 | -13 | -29 |

| Q4 24 | -13 | -16 |

Summary of Special Questions

Firms were asked what oil and natural gas prices were needed on average for drilling to be profitable across the fields in which they are active. The average oil price needed was $62 per barrel (Chart 2), while the average natural gas price needed was $3.69 per million Btu (Chart 3). Firms were also asked what prices were needed for a substantial increase in drilling to occur across the fields in which they are active. The average oil price needed was $84 per barrel (Chart 2), and the average natural gas price needed was $4.66 per million Btu (Chart 3).

Firms reported what they expected oil and natural gas prices to be in six months, one year, two years, and five years. The average expected WTI prices were $70, $71, $75, and $81 per barrel, respectively. The average expected Henry Hub natural gas prices were $3.09, $3.36, $3.67, and $3.98 per million Btu, respectively.

Firms were asked about their plans for employment and capital expenditures in 2025 vs. 2024 (Chart 4). Most firms plan to keep employment levels mostly unchanged (43%) or increase them slightly (40%). Another 10% of firms plan to increase employment significantly, and only 7% plan to decrease employment slightly. Plans for capital expenditures were more mixed. Many firms plan to increase capital expenditures slightly (43%), while 17% plan to increase them significantly, 13% remain unchanged, 17%, decrease slightly, and 10% decrease significantly.

Contacts were also asked about other future plans (Chart 5). 52% of firms plan to reduce methane emissions, 35% plan to reduce flaring, 32% plan to recycle/reuse water, 26% plan to reduce CO2 emissions, and 10% plan to invest in renewables, while 32% have none of the above planned.

Chart 4. Special Question: What are your expectations for your firm's employment levels/capital spending in 2025 vs. 2024?

Skip to data visualization table| Category | Employment | Capital Spending |

|---|---|---|

| Increase significantly | 10 | 17 |

| Increase slightly | 40 | 43 |

| Remain close to 2024 levels | 43 | 13 |

| Decrease slightly | 7 | 17 |

| Decrease significantly | 0 | 10 |

Chart 5. Special Question: Which of the following plans does your firm have? (Check all that apply)

Skip to data visualization table| Category | Percent |

|---|---|

| Reduce methane emissions | 52 |

| Reduce flaring | 35 |

| Recycle/reuse water | 32 |

| Reduce CO2 emissions | 26 |

| Invest in renewables | 10 |

| None of the above | 32 |

Selected Energy Comments

“At this point, the high cost of capital along with inflation are our only significant concerns.”

“Commodity pricing and inflation will control activity. Activity levels are not hypersensitive to either but changing trends will impede or accelerate activity.”

“Long term, companies will not make the money they need at sub $70 oil and therefore capex will fall off, leading to lower domestic and international production then to slightly increasing prices.”

“At sub $3.25 Henry Hub, companies are not profitable enough to continue development.”

“Build-out of LNG is also supporting price recovery.”

“We can deliver as much gas as country needs at $3.50 prices. LNG ramp up raises U.S. price and drops worldwide price.”

“Disassociated gas in west Texas trades for less than $1.00/mcf.”

“Strong rig response from any price lift.”

“We are currently reusing produced water for frac water. We are increasing our methane monitoring.”

“Wind project is underway on some of our land holdings.”