Farm income and loan repayments rates recovered from sharp declines in the second quarter, and demand for credit softened according to Federal Reserve District Ag Credit Surveys. Although farm income generally remained low, rates of loan repayment stabilized, and farmland real estate markets remained strong.

Third Quarter Federal Reserve District Ag Credit Surveys

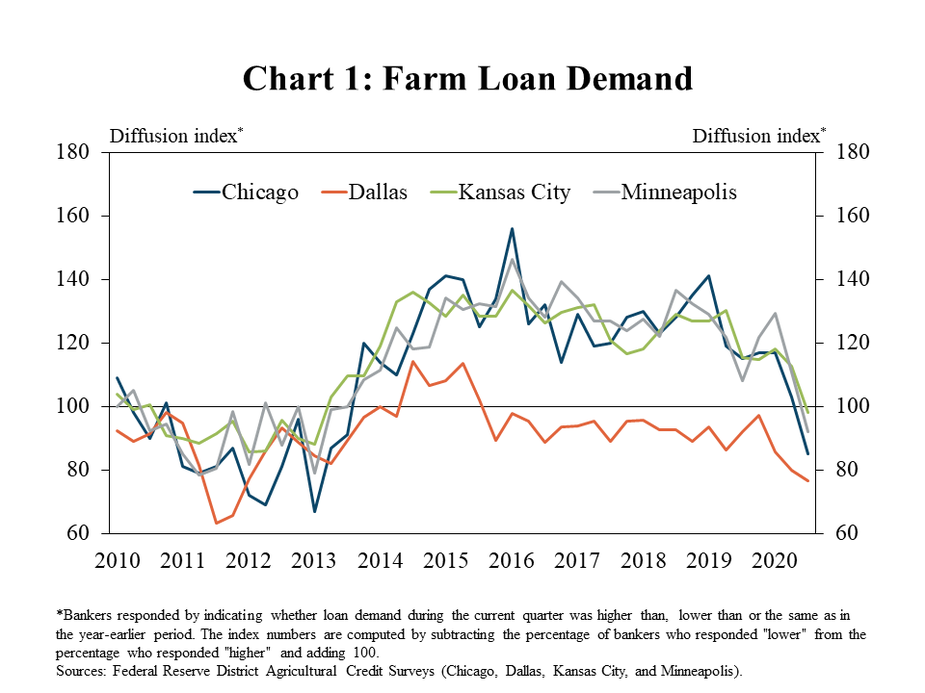

Farm loan demand moderated in all Federal Reserve districts for the first time since 2013 in the third quarter. Although a majority of bankers in the Dallas District have reported lower lending activity since 2016, the third quarter was the first time in seven years that bankers reported a decline in the credit needs of farm borrowers in all districts (Chart 1).

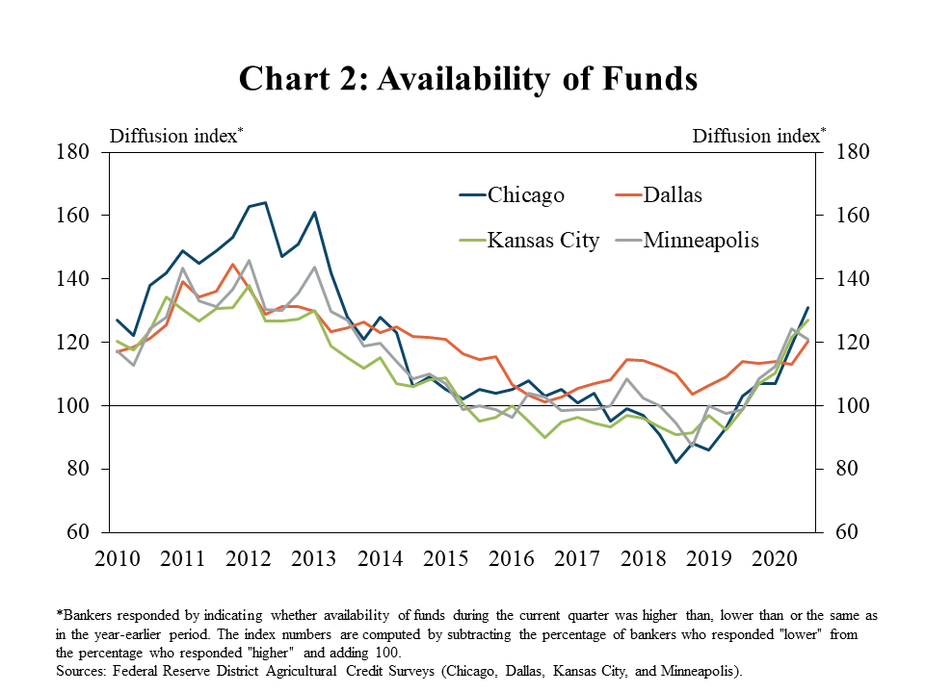

The pace of growth in available funds, however, continued to increase in most districts. In all Districts, funding at agricultural banks was likely supported by higher deposits and an influx of liquidity from Federal Reserve and government programs following the outbreak of COVID-19 (Chart 2). In fact, in the second quarter, 85% of bankers in the Kansas City District reported that deposits were higher than a year ago.

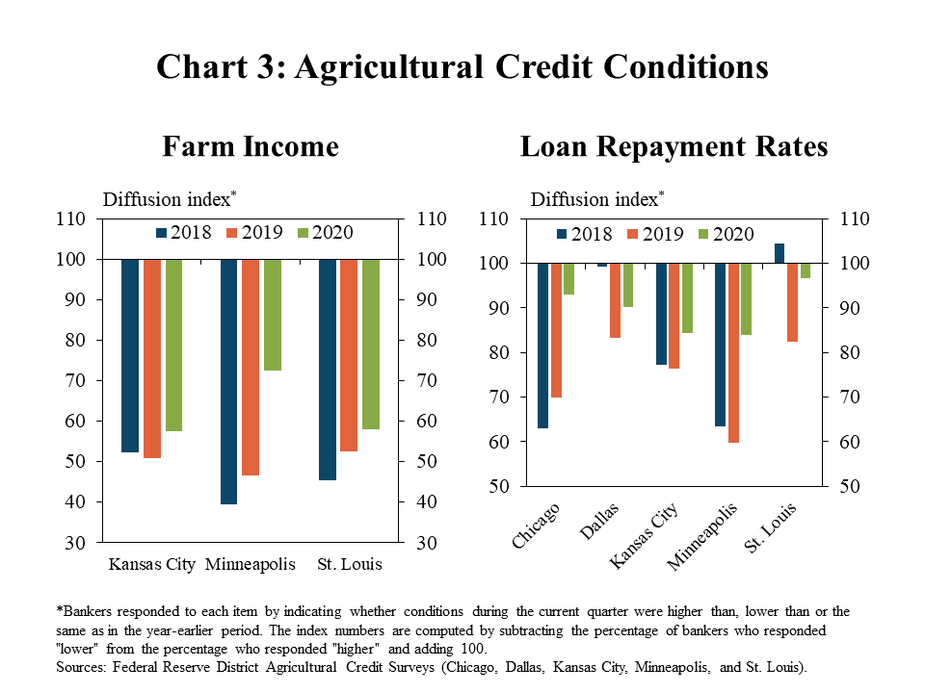

Alongside reduced lending activity, agricultural credit conditions improved somewhat in the third quarter. Although most bankers continued to report that farm income and repayments rates were lower than a year ago, the pace of decline slowed in all districts (Chart 3). Compared to last year, farm finances seemed to stabilize the most in the Chicago and Minneapolis districts, where corn and soybeans make up a larger share of farm revenues.

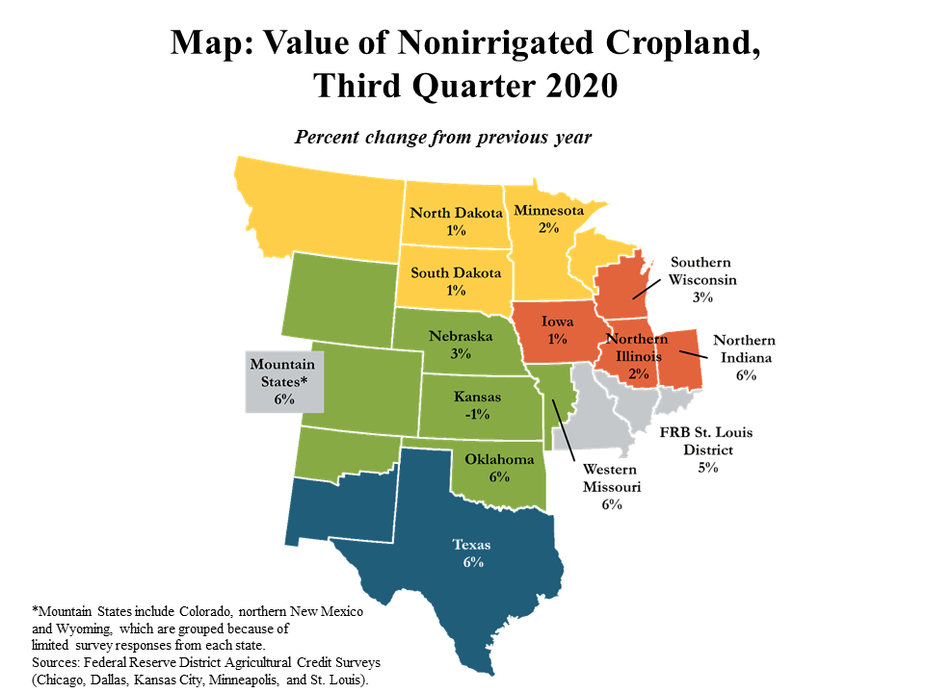

Farmland values generally remained strong across all regions. Values for nonirrigated cropland increased or remained stable in all reporting states and districts (Map). Gains in land values were most pronounced in states located in the lower Midwest and southern Plains.

Conclusion

An influx of government payments and higher prices for agricultural commodities provided greater support for farm finances in the third quarter and seemed to limit demand for financing. Despite some improvements in the agricultural economy, farm income and repayment rates remained low, albeit not as low as in the second quarter. Increased uncertainty related to the pandemic may also have curbed some demand for new loans and could continue to weigh on agricultural lending conditions moving forward.

Data and Information

Federal Reserve Ag Credit Surveys Historical Data

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author