Insights on Agricultural and Rural Economies

Regular updates and concise analysis on agricultural and rural economic trends from the Center for Agriculture and the Economy.

Disclaimer

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Drought is an Increasingly Important Factor for Many Agricultural Products

Drought risk has expanded and intensified in recent months and could materially affect production, markets, and revenues for many commodities and producers across key agricultural regions. About 60% of U.S. cattle inventories and hay acreage have been in at least moderate drought since early April, which is the highest two-month average since 2022 (top chart). Winter wheat exposed to drought also reached the highest level since 2022, while the average share of rice, peanuts and cotton in drought over that time increased to more than 90%, the highest since at least 2000 (bottom chart). In addition to the commodities shown below, drought has also persisted in western states where many specialty and permanent crops are prominent.

Notes: The calculations represent the portion of each commodity exposed to drought categorized as D1-D4 (moderate, severe, extreme, and exceptional) based on the intensity classifications used by the External LinkUniversity of Nebraska – Lincoln U.S. Drought Monitor. The calculation for cattle is based on the share of cattle inventories in areas experiencing drought categorized as D1-D4. The calculation for hay is based on the share of acreage in areas experiencing D1-D4 drought. The calculation for rice, peanuts, cotton, winter wheat, corn, and soybeans is based the share of production in areas experiencing D1-D4 drought. Rice, peanuts, and cotton is the average for all three individual crops and corn and soybeans in the average for both crops.

Source: USDA, University of Nebraska- Lincoln National Drought Mitigation Center, and Federal Reserve Bank of Kansas City Staff Calculations.

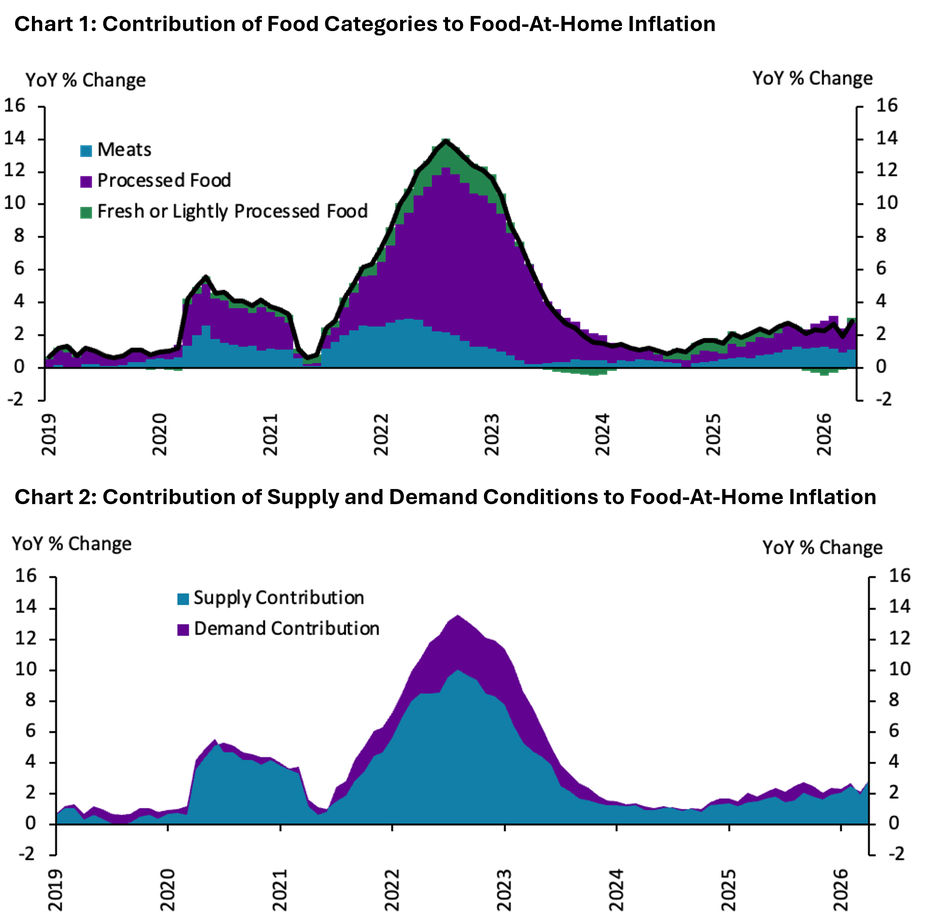

Grocery Prices Are Inching Higher from Supply Conditions in Meat and Processed Foods Sectors

Food prices have increased at a faster pace in 2026 than in 2025, but at a slower pace than the peaks of the last five years (Chart 1). Inflation in prices for food consumed at home (i.e., food-at-home inflation) peaked in 2022 at an average yearly rate of 11.7%, driven by increases in the prices of meat and processed food, but eased to an average of 2.2% in 2025. Higher meat and processed food prices have again driven most of the food-at-home inflation in 2026, which registered a 2.8% increase in prices this April compared to the same period last year.

Changes in supply conditions have explained most of the increase in prices for food at home in 2026. Unlike the post-pandemic period, when strong consumer demand explained a sizable portion of US food-at-home inflation, increasing pressures on the food supply chain have explained most of the current variation in food prices (Chart 2). Evolving cost pressures in the processing, wholesale, retail, and transportation sectors, together with constrained supply of cattle herd liquidation and the slow pace of herd rebuilding in recent years, have increased the contribution of sectors with more complex supply chains, such as meat and processed foods, to inflation. As discussed in Cowley and Scott (2022), these supply factors tend to have a large effect on food prices.

Overall, supply conditions affecting meat and processed foods have contributed the most to increases in food-at-home prices. Without changes in demand for these types of foods, easing supply pressures may help soften the increases in food-at-home prices.

Chart 1

Note: Processed food includes cereal and baked goods, cheese, ice cream, other dairy products, processed fruit and vegetables, beverages, and the category of other food at home. Fresh and lightly processed food includes eggs, milk, and fresh produce. Meats includes all meat products.

Sources: Bureau of Economic Analysis, and author’s calculations

Chart 2

Notes: We use the following aggregate categories from the PCE to decompose food inflation into demand and supply shocks: cereal and bakery, meat and poultry, fish and seafood, milk, dairy and eggs, fats and oil, fresh fruits and vegetables, processed fruits and vegetables, sugar and sweets, other food products, and nonalcoholic beverages. The full decomposition methodology can be found in Shapiro (2026).

References: Shapiro, Adam Hale. "Decomposing Supply‐and Demand‐Driven Inflation." Journal of Money, Credit and Banking 58, no. 2 (2026): 365-388.

Cowley, Cortney, and Francisco Scott. "Commodity Prices Have Limited Influence on US Food Inflation." Federal Reserve Bank of Kansas City, Economic Bulletin, September 23 (2022).

Sources: Bureau of Economic Analysis, and author’s calculations

The U.S. Farm Economy Has Outperformed Pre‑Pandemic Expectations

Economic conditions in agriculture have softened in recent years but remain notably stronger than what was expected prior to the pandemic. In 2019, USDA projected that farm income would remain subdued over the next 10 years due, in part, to expectations of strong global production of major row crops and limited demand growth. Instead, from 2020 through 2025, farm income was almost $300 billion higher, cumulatively, than what 2019 projections anticipated. Government payments accounted for $70 billion of this total. Although farm income has fallen from a near-record high in 2022, the post-pandemic strength has continued to provide support during the recent downturn.

Sources: USDA and Federal Reserve Bank of Kansas City staff calculations

Risks From Disruptions in Global Fertilizer Markets Vary Across the U.S. and Brazil

The level of exposure to disruptions in global fertilizer markets from conflict in the Middle East varies across the U.S. and Brazil given their respective import dependence, trade partners, and long-term trends in fertilizer use. The U.S. produces the majority of its fertilizer domestically with dependence on critical inputs limited to nearby trade partners like Canada and Peru. Brazil, on the other hand, depends almost entirely on imported fertilizer from trade partners that include Iran, Qatar, and Saudi Arabia who rely on the Strait of Hormuz for transit. While producers in both countries face higher prices, those in Brazil face greater near-term risk of fertilizer shortages and consequently lower production.

In the United States, growth in corn and soybean yields has largely outpaced fertilizer use over the last 25 years due to improvements in plant genetics and innovations in nutrient management. By contrast, gains in Brazilian corn and soybean yields over time have been fueled by more intensive fertilizer use. This is particularly true for corn where the cost of fertilizer per bushel in Brazil is a higher component of operating costs than in the U.S. As such, any persistence in higher fertilizer prices over 2026 and 2027 implies tighter profit margin compression for Brazilian producers.

Note: Corn and soybean yield for the U.S. and Brazil depict the metric tons harvested per hectare of land used in the cultivation for each crop. Fertilizer use refers to total fertilizer consumption across nitrogen, phosphorus, and potassium fertilizers in kilograms per hectare of arable land.

Sources: USDA Production, Supply and Distribution Statistics; Food and Agriculture Organization of the United Nations

Input Prices in Food and Energy Sectors Rose Sharply in April

Although prices for inputs rose at most manufacturing and services firms in April, the pace of increase in prices was faster for firms in the food supply chain. Input prices in energy and chemical sectors, which produce and distribute products for agriculture and other industries, also rose at a rapid pace. The index for the price of raw materials among food, energy, and chemical manufacturers rose from 29 in March to 74 in April, which was the fastest rate of increase since February 2022 (blue line in the left panel). In the services sector, the index for input prices at grocery stores, restaurants, and gas stations (blue line in the right panel) has remained comparably higher than other establishments in recent years and increased sharply in April even as the index was relatively steady at other firms. Contacts reported that recent cost pressures were primarily due to increases in transportation expenses related to a spike in freight and fuel prices and many also mentioned it was getting increasingly difficult to pass cost increases on to customers.

Note: The diffusion index is calculated as the percentage of total respondents reporting increases minus the percentage reporting declines. The data shown are seasonally adjusted.

Source: Federal Reserve Bank of Kansas City Business Surveys

Population Has Declined in Farming Dependent Counties Since the Pandemic

Since 2020, farming-dependent counties were the only major county typology where population growth has been negative. There has, however, been significant variation in population growth across farming dependent counties. The most sluggish county, Tallahatchie Co., Mississippi, lost more than 1,700 residents from 2020 to 2025 (15% of its population). Over the same time frame, Jerome Co., Idaho gained more than 2,000 people (8% of its population). Maintaining population is crucial for many reasons, including ensuring the steady supply of local labor, preserving local tax bases, and sustaining demand for goods and services provided by local businesses. Counties with notable declines could be more exposed to potential economic challenges.

Note: County dependencies are mutually exclusive and defined by External Linkthe USDA. Counties with “no dependence” are not reliant on any industry in particular.

Sources: USDA, Census Bureau, and Federal Reserve Bank of Kansas City staff calculations

Agricultural Borrower Conditions Remain Stable

By: Tony Mancinelli, Phil Shafer, and Chris Summers

Despite persistent weakness in the crop sector, noncurrent rates on farm loans at commercial banks remained stable through the fourth quarter of 2025. According to anecdotal information from recent bank examinations, notable deterioration has not emerged for row crop farmers. Producers have improved operational efficiencies through expense reduction, revenue diversification (trucking, custom work, marketing), and careful machinery line management. Record 2025 corn and soybean yields, and one-time Farmer Bridge Assistance (FBA) program payments helped buoy farm incomes and offset production cost pressures. Cattle producers have continued to benefit from strong prices, and some banks have reported record-low problem asset levels among cattle operator concentrations.

Notes: Noncurrent includes loans 90+ days past due or on nonaccrual. Community banking organizations (CBOs) are defined as commercial banks having less than $10 billion in assets. Agricultural banks are defined as commercial banks with agricultural production and farm real estate loans equaling 25 percent or more of total loans. Highly concentrated agricultural banks are defined as commercial banks with agricultural production and farm real estate loans equaling 300 percent or more of tier 1 capital plus the allowance for credit losses (ACL). This more stringent definition captures approximately the top one-third of all agricultural banks.

Source: Reports of Conditions and Income

Tony Mancinelli, Phil Shafer, and Chris Summers are supervisory examiners at the Federal Reserve Bank of Kansas City.

Crop Farmers Could Face Slight Profit Margin Compression After Disruptions in the Strait of Hormuz

Disruptions at the Strait of Hormuz have driven up production costs for U.S. crop farmers, even as higher commodity prices created profit opportunities for some. From early February to late March, urea prices, a key source of nitrogen fertilizer, rose about 50%, and diesel prices increased more than 45%. As planting season approaches, input price hikes could squeeze profit margins, especially if cost increases outweigh the nearly 10% gain in December corn futures prices since the beginning of the year.

Some producers are likely to see a slight decline in profit margins due to the disruption, particularly those who have not prepaid or contracted fertilizer. Before March, USDA forecasts suggested that the cost of producing a bushel of corn would exceed average corn prices by $0.07 in 2026. As of mid-March, this gap has likely widened to $0.12 per bushel. Average expected margins have declined alongside higher fertilizer expenses, rising energy costs, and slightly lower yields due to reduced nitrogen application. The recent distribution of government payments could alleviate some pressure on producers, but prolonged disruptions could further strain the supply of energy and fertilizers and influence farmer decision making in future years.

Note: Corn breakeven prices are calculated from USDA’s “Cost and Returns” for 2021 to 2026F, and exclude opportunity cost of labor. Corn prices for 2026 are based on futures prices and set to $4.67/bu before the disruptions, and $4.88/bu in March 2026. We use Iowa State University’s “Estimated Costs of Crop Production” to obtain prices and quantity used of N fertilizer for a typical corn-corn rotation for 2026 before the disruption. We update the price of nitrogen (N) fertilizer for March 2026 based on the increase in urea prices at the Gulf. We assume that farmers adjust N application based on N fertilizer price changes and use the supply disruption from the Russia-Ukraine war to identify the sensitivity of aggregated U.S. N use to prices (elasticity of -0.115). We then use a rule-of-thumb of 1 bu/acre reduction in corn yield from a 1 lbs/acre decrease in N application to update corn yields for March 2026 (Enrria et al., 2024). Finally, we update energy costs in March 2026 based on the percentage increase in Brent crude oil prices and the pass through rate of oil prices to energy prices from Känzig (2021) (elasticity of 0.45).

Sources: USDA, International Fertilizer Association, Iowa State University, Enrria et al. (2024), Känzig (2021), and author’s calculations

Disruptions in the Strait of Hormuz Pressure Fertilizer Prices Ahead of the U.S. Growing Season

Producers currently purchasing fertilizer ahead of the planting season are facing significant cost increases given the ongoing conflict in the Middle East. The Strait of Hormuz is a key shipping channel for globally traded fertilizers. Notably, more than a third of global exports of urea, a widely used solid nitrogen fertilizer, typically pass through this waterway. Since the beginning of the year, the price of urea has increased by about 55%, sharply rising with the onset of conflict with Iran.

As a nitrogen-intensive crop, fertilizer purchases comprise a large component of corn production expenses. As such, corn growers face higher input costs with supply shocks in the urea market. Urea markets have already been under pressure from persistently high natural gas costs alongside the Russia-Ukraine war and export restrictions from China. At present, the relative price of urea, or implied trade-off between corn and urea, is close to the record high experienced in 2021 amidst natural gas supply disruptions. However, recent increases in the price of corn may support profitability. In addition, many producers secured fertilizer for this year’s growing season last Fall ahead of the surge in prices. Going forward, developments in global urea markets and movement in commodity prices will be important for evaluating the outlook for corn profitability.

Note: The relative price of urea to corn is calculated as the ratio of the Urea U.S. FOB Gulf $/Ton to the Chicago Mercantile Exchange’s 1st Expiring Contract Settlement Corn Futures Price, with cents/bu converted to $/bu.

Data Sources: Bloomberg and Haver.

The Number of Cattle Processed into Beef Has Declined Alongside Low Inventories and Reduced Slaughter Capacity

U.S. beef cattle slaughter has continued to deviate from the pre-pandemic baseline in early 2026. During 2020 and 2021, shocks associated with COVID-19, severe weather, and a cyberattack at JBS contributed to substantial disruptions in the beef supply chain. Similarly, in November 2025, the total number of cattle slaughtered in the U.S. was 22% lower than in January 2020. However, more recent deviations in cattle slaughter have not resulted from shocks in the supply chain but from historically low cattle inventories. As cattle inventories have declined, higher procurement costs and lower capacity utilization have created challenges in the beef packing industry and contributed to reduced hours for workers and closures at three beef packing plants in early 2026. Moving forward, reduced slaughter capacity will likely boost efficiency in the supply chain but keep beef production at lower levels.

Note: Calculations based on the total number of cattle, greater than or equal to 500 pounds, that are slaughtered in commercial meat packing facilities in the United States.

Sources: U.S. Department of Agriculture (USDA) and Federal Reserve Bank of Kansas City staff calculations

Mass Layoff Events Occur Less Frequently in Rural Areas but Tend to Have a Larger Impact

A recent meatpacking plant closure in Lexington, Nebraska has highlighted the severe, negative consequences of large employment disruptions on small communities. A recent Economic Bulletin provides an overview of these expected consequences with a particular focus on Lexington. Existing literature suggests that smaller, more economically concentrated communities might face larger negative consequences than larger, more economically diversified areas. As the charts below show, mass layoffs have occurred less frequently in rural areas but those occurrences, on average, tend to affect a much larger share of the local labor force.

Mass Layoff Events Announced through WARN Notices Since 2000

Note: right hand chart includes only those WARN notices impacting at least 100 workers where the location of the layoff is in a single location and where the location is easily identifiable. On average, about 16% of notices per year affect multiple locations or do not have easily accessible geographic information. The WARN Act requires employers with at least 100 employees to provide advance notice of employment disruptions under External Linkcertain criteria.

Sources: warntracker.com and Federal Reserve Bank of Kansas City staff calculations

USDA’s Net Farm Income Projections Reflect New Timing of Government Transfer and Weaker Revenues in Parts of the Livestock Sector

Estimates from the United States Department of Agriculture (USDA) showed a decline in net farm income for 2025 of more than $25 billion from the previous projection. The timing of government payments previously expected during 2025 were responsible for most of the decline. Lower than expected revenues in the livestock sector, particularly for poultry and eggs and small upticks in feed, fertilizers, and pesticides expenses pulled net farm income lower than projected in September of last year. Crop revenues slightly offset the declines, as the USDA estimated oil crop revenues in 2025 to be stronger than previously projected.

Initial projections by the USDA indicate that net farm income may decline by 2.6% ($4 billion) in 2026 compared to last year. Government payments are expected to continue to contribute positively to net farm income, totaling $42 billion, as some direct transfers planned for 2025 will likely be paid in 2026. Projections show operational expenses softening slightly, while livestock revenues may increase moderately, which could help pull net farm income higher. However, the USDA projects lower revenues from crops, dairy, and poultry and egg production, which may offset some of the projected savings on inputs and expected gains from other sectors.

Source: USDA, staff calculations.

Demand for Stable Access to Water Has Supported a Rise in the Price Differential for Tenth District Irrigated Farmland

According to fourth quarter results from the Tenth District Survey of Agricultural Credit Conditions, land values remained stable in 2025, with a premium for irrigated farmland. In fact, the price differential between irrigated and non-irrigated farmland has increased five-fold in the last two decades. The rise in the premium for irrigated farmland has been supported by heightened demand for stable access to water given more severe droughts, depletion of existing water resources, and the pursuit of higher yields. Rather than large-scale expansion of irrigated acreage, mounting concerns about water scarcity have altered investment decisions and production practices towards the adoption of more efficient irrigation technology and shifting regional cropping patterns.

Note: The premium for irrigated farmland is calculated as the difference between the survey average of irrigated and non-irrigated land values (per acre). This difference is indexed to 2025 to account for inflation. Exceptional drought refers to the highest intensity level on the U.S. Drought Monitor, indicating a 1-in-100-year event.

Sources: Federal Reserve Surveys of Agricultural Credit Conditions; National Integrated Drought Information System’s U.S. Drought Monitor.

High Production Costs and Subdued Liquidity Spurred Strong Farm Lending Activity in 2025

Estimates from the National Survey of Terms of Lending to Farmers showed a 20% year-over-year increase in the average inflation-adjusted volume of new farm operating loans at commercial banks during 2025. Demand for financing grew considerably for the second consecutive year alongside elevated production expenses and subdued liquidity in the sector, particularly for crop producers challenged by narrow profit margins. The latest Ag Finance Update describes how the growing size of operating loans continued to drive increases in lending volumes over the past year.

*Average annual volume of loans for current operating expenses estimated in the Survey of Terms of Lending to Farmers.

**Total U.S. farm sector production expenses less interest expenses and capital expenditures.

Sources: USDA, Survey of Terms of Lending to Farmers, Federal Reserve Bank of Kansas City and Federal Reserve Bank of Kansas City staff calculations

Artificial Intelligence Could Be Useful for Increasing Productivity and Managing Labor Costs in the Agricultural Sector

Like other industries, agricultural businesses employ individuals whose labor could be enhanced with Artificial intelligence (AI). The share of current employment in agriculture exposed to AI varies across states and is influenced by differing labor requirements among farm products. In regions like the Midwest and Plains, agriculture concentrated in row crop production requires relatively few employees and a greater share of labor could be enhanced with the use of AI. Conversely, the prevalence of specialty crop production in California and Florida requires more in-field farm workers that could limit the benefits of AI.

Note: The map follows calculations described in the December 2025 Nebraska Economist (External LinkMcCoy 2025). Employment includes agriculture, forestry, fishing, and hunting industries.

Sources: Eloundou et al (2024), Census Bureau (American Community Survey), author’s calculations.

Government Assistance and Insurance Payouts Will Limit Losses for Some Crop Farms

Profit opportunities in the crop sector remained limited at the end of 2025, but the combination of ad hoc government assistance and expected crop insurance payouts is likely to support farm financial conditions. A hypothetical analysis estimates a corn and soybean farm with average U.S. yields, selling at average annual cash prices will lose $80 per acre in 2025. If these conditions persist in early 2026, those losses could be cut in half with disbursements from the Farmer Bridge Assistance (FBA) Program and mostly offset with payments from revenue and price protection programs. The level of direct support is notable compared with recent years and together with aid from the Emergency Commodity Assistance Program (ECAP) earlier this year, could ease financial stress for many crop producers.

Note: Profits are based on production costs from the USDA cost and return estimates and national average yields and prices. For purposes of this analysis, the opportunity cost of unpaid labor is excluded from total costs. Government payments from 2010-2023 are estimated using average government payments per farm for corn and soybean specialized operations reported in the Agricultural Resource Management Survey (ARMS). Estimated payments from FBA and ARC/PLC in 2025 are derived from analysis published by University of Illinois at Urbana-Champaign.

Sources: USDA, Wall Street Journal, Reports of Condition and Income, University of Illinois at Urbana-Champaign, and Federal Reserve Bank of Kansas City staff calculations