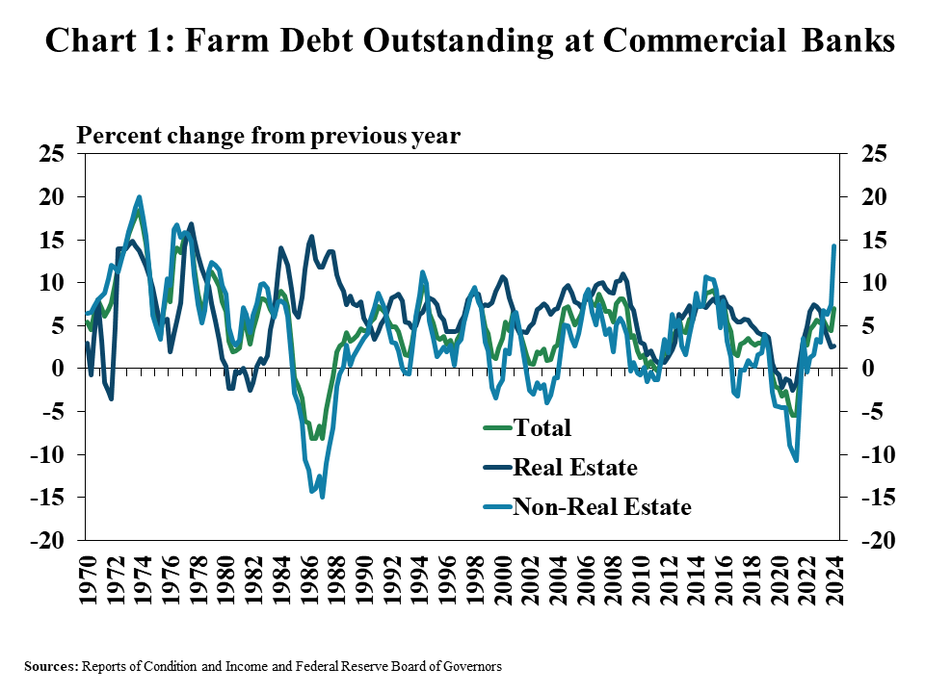

Farm debt at commercial banks continued to grow at a steady pace from the year prior boosted by a substantial increase in farm operating debt. The growth in real estate debt remained robust but down from the peaks observed in early 2023. Overall, agricultural banks remained financially stable despite a slight increase in farm loan delinquency rates.

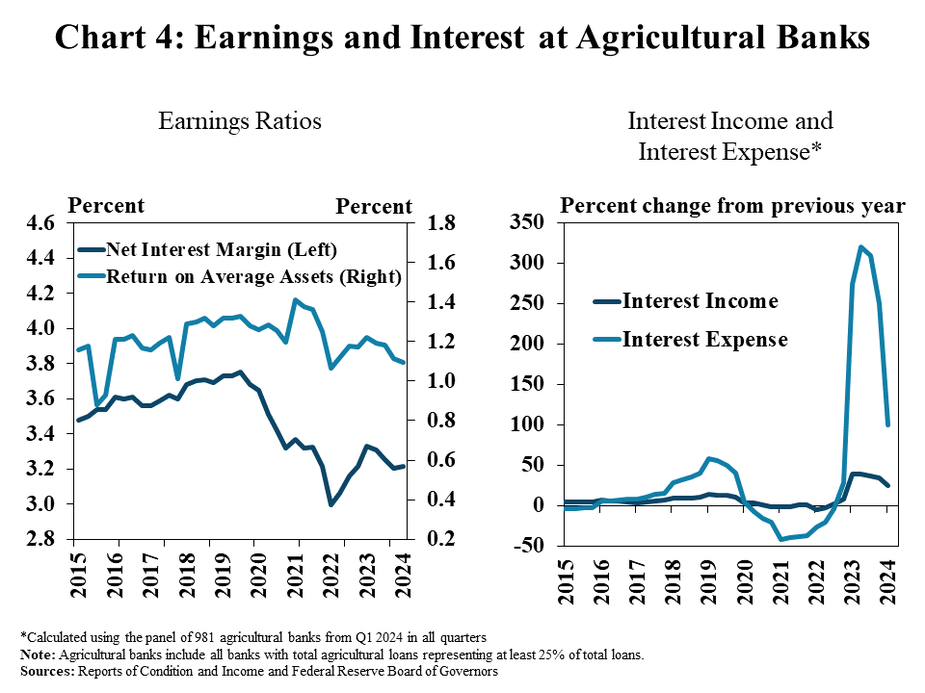

The strong growth in farm operating debt in the first quarter reflects an increase in farmers’ financing needs, which had been subdued since 2021. The uptick in demand, along with higher benchmark interest rates, resulted in a substantial increase in yields for these loans and higher interest earnings for agricultural banks. However, margins for agricultural banks increased only modestly as the growth in interest income was partly offset by higher interest expenses.

First Quarter Commercial Bank Call Report Data

Substantial growth in agricultural production loans boosted farm debt balances. Non-real estate farm loans at commercial banks ended the first quarter nearly 15% higher than a year ago, the largest increase since the late 1970s (Chart 1). The rapid increase in operating debt boosted total agricultural debt even as farm real estate debt increased only modestly.

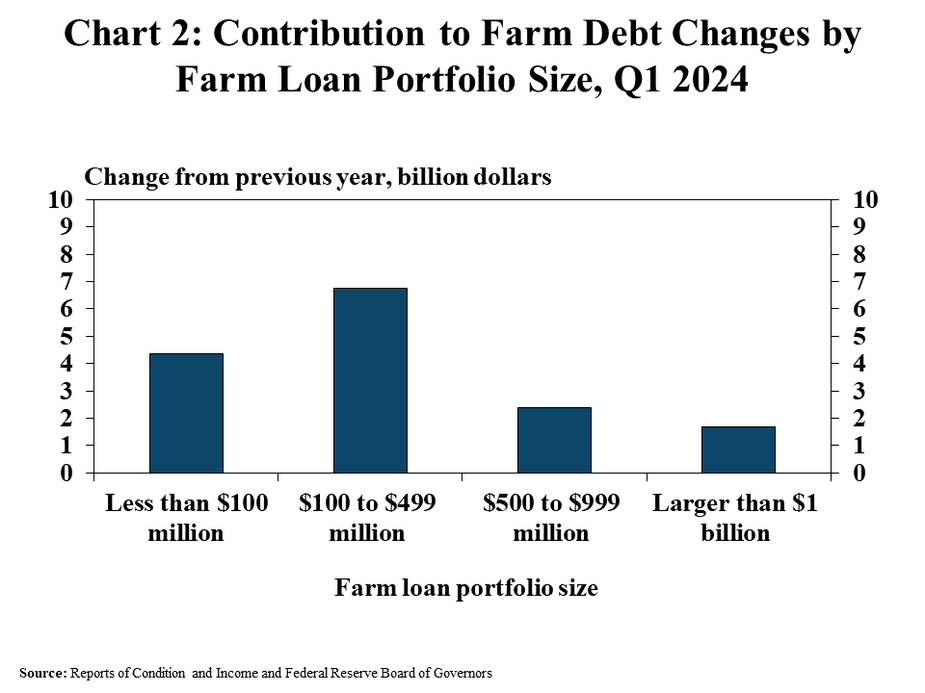

The growth in agricultural debt was concentrated among small and mid-sized farm lenders. Three quarters of the $15 billion increase in farm debt was attributed to banks with agricultural loan portfolios less than $500 million (Chart 2). The largest lenders with portfolios over $1 billion accounted for about 10% of the growth.

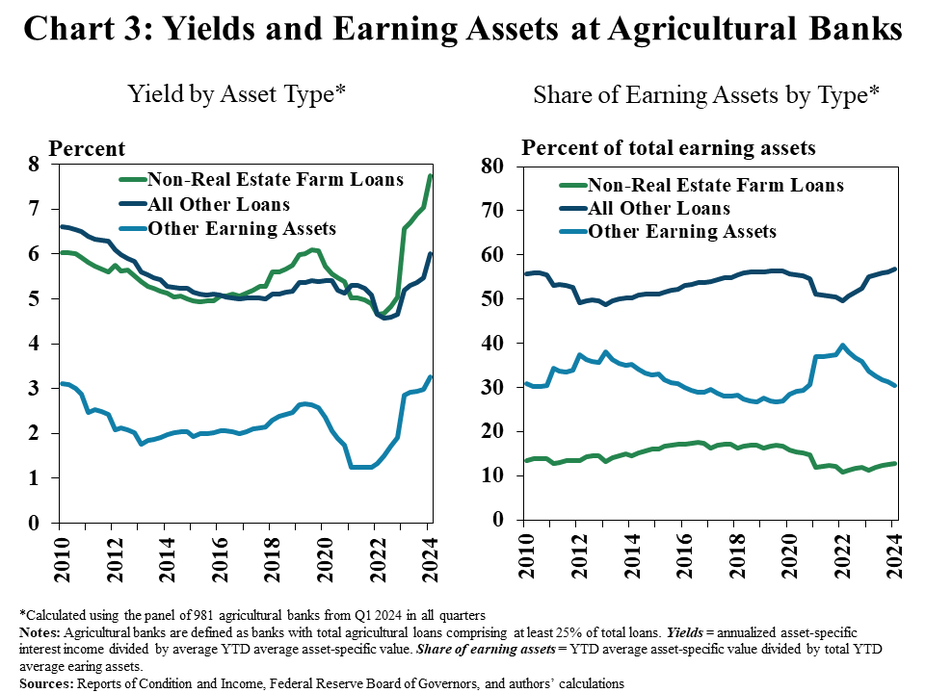

Alongside strong loan demand and higher benchmark interest rates, yields on farm operating loans have grown considerably at agricultural banks. Yields on farm operational loans increased by more than 1 percentage point from the previous year, surpassing the growth in yields for other assets (Chart 3). Agricultural banks continued to expand their loan portfolio, replacing lower-yielding assets on their balance sheet.

Even as farm loan yields have risen, the growth rate in interest expense continued to outpace income and limit margins for agricultural banks. As benchmark rates have increased in recent years, interest expenses for many community banks have risen faster than interest income and put some pressure on net interest margins (Chart 4). Profits have remained solid despite tight margins, and the recent demand for higher yielding farm operating loans could provide support to interest income going forward.

Data and Information

Excel SpreadsheetCommercial Bank Call Report Historical Data

Excel SpreadsheetCommercial Bank Call Report Data Tables

txtAbout the Commercial Bank Call Report Data

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.