The COVID-19 pandemic has resulted in some unique dynamics in Oklahoma’s housing sector—and more attention on housing in general—as many residents are spending more time in their homes than ever before. On one hand, even as higher unemployment, consumer caution and business restrictions wreaked havoc on some sectors in 2020, Oklahoma home sales, prices and construction boomed. This strength has offset some of the weakness in other industries, such as energy and hospitality. At the same time, however, housing insecurity, past-due mortgages and risk of eviction have increased for other Oklahomans. This edition of the Oklahoma Economist reviews these diverging trends and where they may be heading.

Faster growth in sales, prices, and construction

Home sales have surged in 2020, pushing inventories of homes even lower. In November, existing home sales in the United States were up 26% from a year ago, and new home sales had jumped 21%._ By the second week of December, the inventory of homes for sale in Oklahoma City and Tulsa—already low heading into the pandemic—were down more than a third from a year ago, as additional homes were purchased and fewer listings were added to the market._

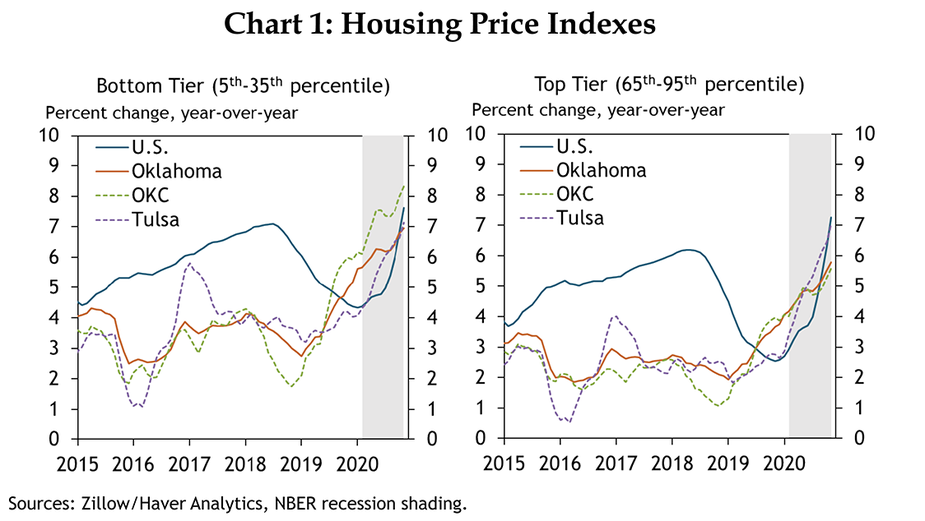

The growth in home prices has been strong across the country, and across home size and price range. The median home price in the United States rose 7.5% from a year ago to $263,351 in November while Oklahoma’s median home price increased 6.8% to $139,409. Home and rental prices routinely have been more affordable in Oklahoma than in the United States, though median wages in the state also have lagged. For the lower-tier, or 5th-35th percentile of home prices in Oklahoma, the median price in November was $67,973, up 7% or more than $4,400 from a year ago, but still less than half the U.S. lower-tier median home price of $137,024 (Chart 1). Price growth for higher-tier homes also increased solidly in 2020, but not quite as much as for lower-tier homes. Prices of homes in the top tier home are up about $15K from a year ago in both Tulsa and Oklahoma City, to $267,021 and $271,550, respectively.

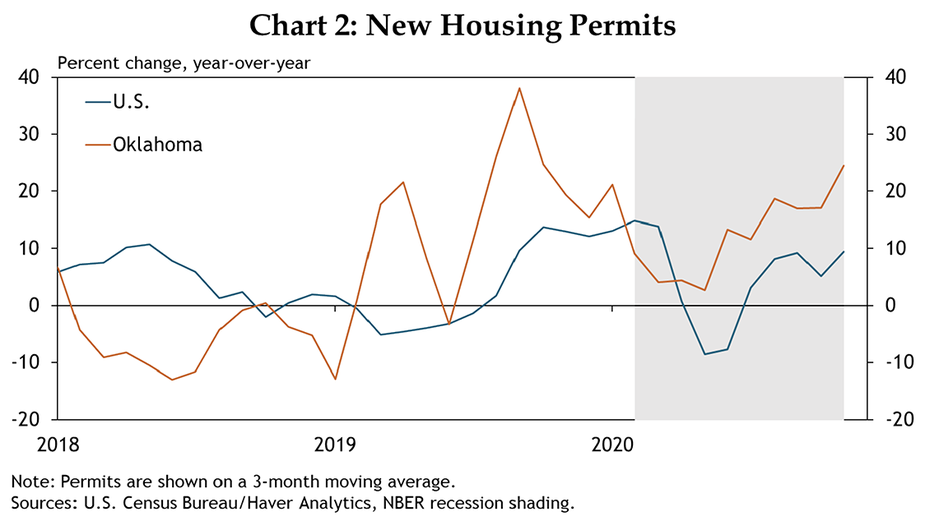

New home construction has also risen markedly. Permits for new privately owned housing units have continued to rise faster in Oklahoma than in the nation (Chart 2). In October, new building permits continued to soar in Oklahoma City but declined slightly in Tulsa compared with a year ago. The number of residential construction employees in Oklahoma also increased 5% in the first half of the year, according to the Bureau of Labor Statistics (BLS).

Several factors boosting Oklahoma housing

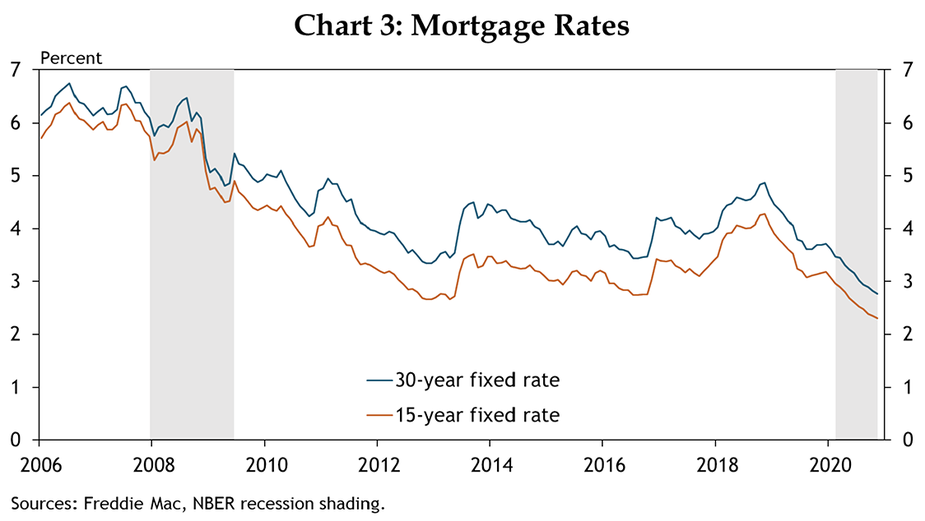

As the global pandemic spread in early 2020, average mortgage rates decreased. Interest rates set by the Federal Open Markets Committee (FOMC) dropped rapidly, making it cheaper for banks to loan money and in turn making loans more available and affordable for consumers, including loans for housing. By November, the average 30-year fixed rate mortgage was 2.8%, significantly lower than the average rate of 7.5% from the last 40 years and down almost a full percentage point from the previous year (Chart 3). The average rate for a 15-year fixed rate mortgage was just 2.3% in November.

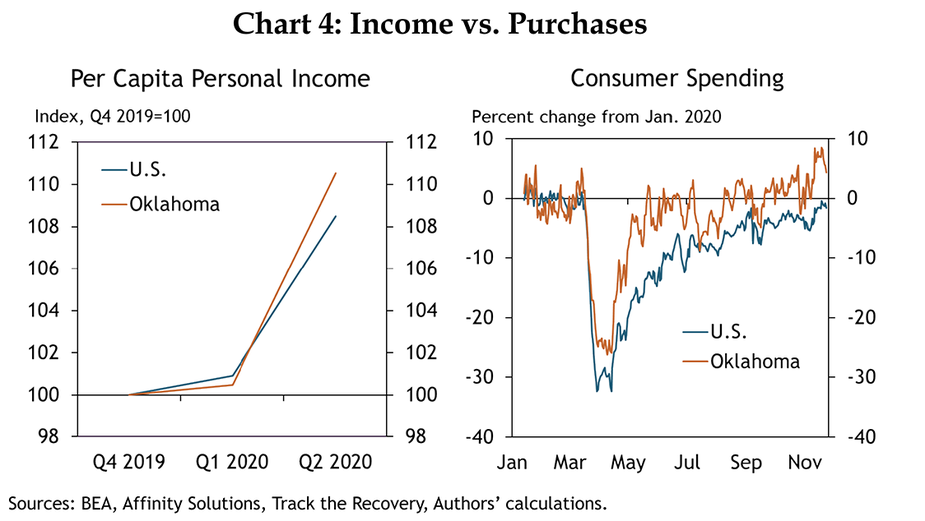

At the same time, despite very high unemployment following the onset of the pandemic, per capita personal income increased more than 10% in Oklahoma in the second quarter of 2020 (Chart 4). While consumer spending in Oklahoma has increased somewhat since January, it hasn’t risen as fast as per capita personal income for many in the state. The state’s economy was not hit quite as hard as the nation, even as sizable government pandemic response programs kicked in. Federal $1,200 stimulus payments in April, tax deferrals until July 15, and higher unemployment insurance benefits through the end of July all helped buoy disposable income levels, potentially providing more funds for homebuying.

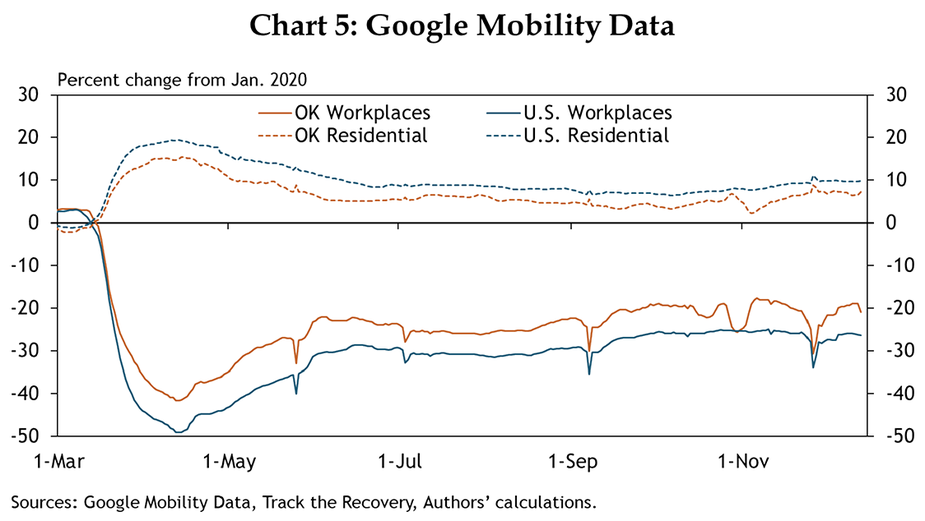

Finally, the demand for additional space increased in 2020 at the same time COVID-19 case counts rose and safer-at-home policies were implemented. Google mobility data shows that Oklahomans stayed at home more and were at their workplace less compared with pre-pandemic times (Chart 5). This was true especially in March and April but remained so through mid-December. As many Oklahomans have continued to work from home or stay at home, this perhaps created different or larger residential real estate needs than in the past.

Challenges, Delinquencies, and Evictions

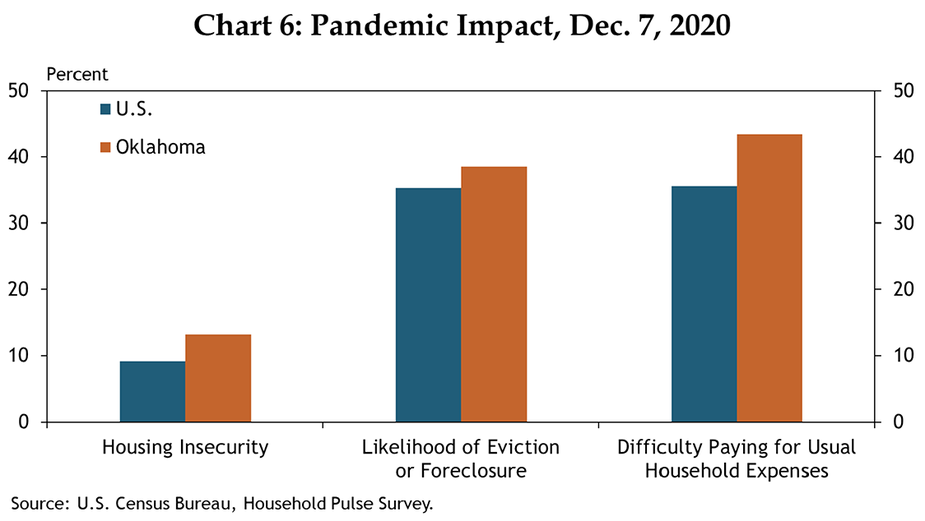

While record low mortgage rates and extra disposable income may have offered many the opportunity to purchase homes and build equity, 2020 job losses and financial worries have contributed to greater housing insecurity for others (Chart 6). Over 35% of those in the U.S. and 43% of Oklahomans surveyed by the U.S. Census Bureau in late November and early December reported “it has been somewhat or very difficult to pay for usual household expenses during the coronavirus pandemic.” This number has risen slightly for several months, indicating continued difficulties as the pandemic continues.

Additionally, nearly 39% of those surveyed in Oklahoma reported their household is not current on rent or their mortgage, or “eviction or foreclosure in the next two months is either very likely or somewhat likely.” Another 13% of Oklahomans surveyed will not be able to pay for another month of housing on time, indicating housing insecurity. In early September, the Centers for Disease Control and Prevention (CDC) took historic action by issuing a nationwide moratorium on residential evictions through the end of December 2020 “to prevent the further spread of COVID-19.”_ The passage of the most recent COVID-19 relief and stimulus package which was signed into law Dec. 27 extended the nationwide eviction moratorium for another month, making it set to expire at the end of January 2021._ The bill also provided $25 billion for emergency rental assistance to be dispersed through states and localities. Despite the temporary respite in housing evictions, over 19,900 eviction filings have been submitted to Oklahoma courts since March 15, with over 7,900 evictions granted._ Moreover, unlike in many areas of the country, rental prices have continued to increase in Oklahoma. Thus, there has been less relief on rental payments for those who rent in Oklahoma, despite sizable job losses.

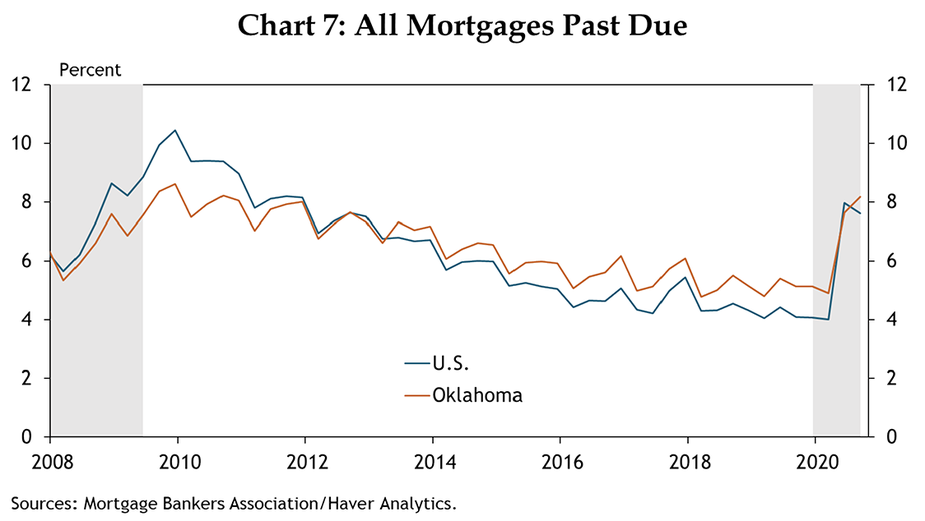

Through the third quarter, mortgage delinquencies in Oklahoma also continued to increase, rising to 8.2%, the highest level since late 2009 (Chart 7). Historically, Oklahoma’s mortgage delinquencies tend to be slightly higher than the U.S. average, but the recent rise has been sharp. Mortgages past due have increased the most for installments 90 days or more past due. In general, delinquent mortgages tend to be higher for Federal Housing Administration (FHA) loans, which frequently are used by low-income and first-time home buyers to secure loans with additional insurance. FHA loan delinquencies have increased in Oklahoma and the U.S. to 14% and 16%, respectively. Current FHA delinquency rates are higher than those observed following the housing crash and the 2008-09 financial crisis.

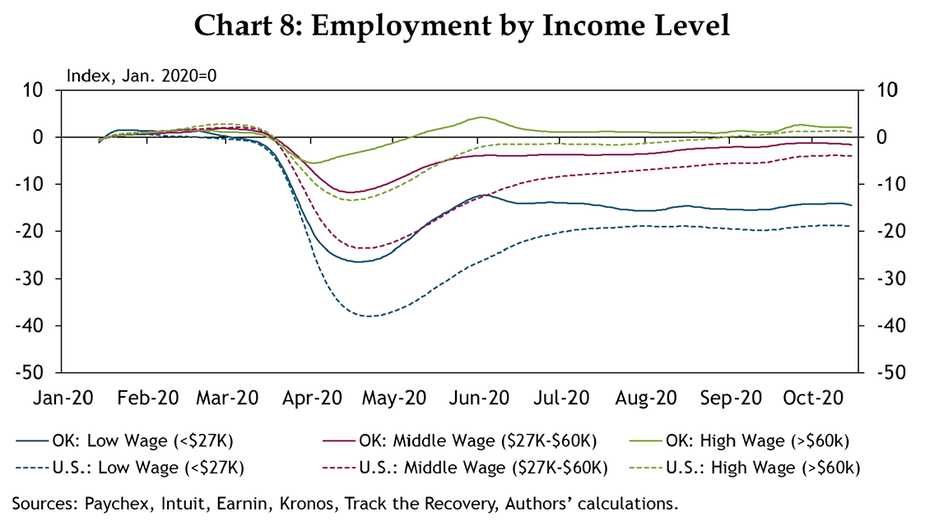

Difficulties paying rent and mortgages could be due to the much higher rate of job losses for lower-income workers during the pandemic. Analysis from the Opportunity Insights Economic Tracker shows that employment rates through mid-October for workers who make less than $27,000 a year were down 15% from January, and employment rates for middle-wage workers who make $27,000 to $60,000 a year were down 2% in Oklahoma (Chart 8). Meanwhile, employment rose slightly for high-wage earners. More jobs have been recovered for each wage sector in Oklahoma than the U.S. average, but employment for low-wage workers still significantly lags employment rates for high-wage workers.

Summary

With more people staying home in Oklahoma and across the nation in 2020, housing has received considerable focus. Many buyers took advantage of low interest rates and greater discretionary income, and sellers were able to increase prices in 2020. Permits for new home buildings also rose substantially. Yet a third of Oklahomans are having difficulties paying household expenses and a significant share are at risk of eviction. Mortgage delinquencies have increased considerably, especially for FHA loans. While the housing sector has been incredibly bright and profitable for many Oklahomans in an otherwise difficult year, the future for others remains cloudy.

Endnotes

-

1 External Linkhttps://www.nar.realtor/research-and-statistics/housing-statistics/existing-home-sales

External Linkhttps://www.zillow.com/research/zillow-weekly-market-report-27151/

-

2 External Linkhttps://www.zillow.com/research/zillow-weekly-market-report-27151/

-

3 -

4 -

5 External Linkhttps://openjustice.okpolicy.org/blog/Oklahoma-court-tracker/

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author