Forecasts for future short-term interest rates are uncertain, and interest rate options markets allow investors to hedge against the risk that interest rates will be higher or lower than projected. For example, if higher-than-projected interest rates would adversely affect a business’s profit, the business may try to protect against this risk by purchasing an options contract that would increase in value should interest rates rise. Similarly, if lower interest rates would negatively affect an investor’s portfolio, the investor may purchase an options contract that would increase in value should interest rates decline. Examining the relative prices of these interest rate options can provide insight into how investors perceive risks to future short-term interest rates.

To formally assess how financial markets perceive the balance of risks to the policy rate, we introduce a new daily measure of policy rate skew. This measure summarizes the relative prices of options that provide upside and downside protection for short-term interest rates one year in the future._ Under our measure of policy rate skew, a positive reading implies investors see a greater risk of higher-than-projected interest rates, a negative reading implies investors see a greater risk of lower-than-projected interest rates, and a reading of zero implies risks are equally balanced between higher and lower interest rates over the next year.

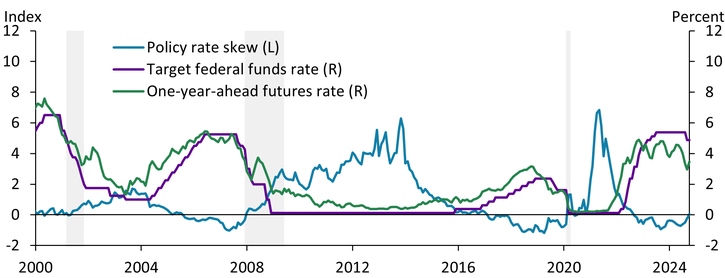

Our measure of policy rate skew tends to lead interest rate cycles, falling and turning negative before the Federal Open Market Committee (FOMC) reduces the target federal funds rate. Chart 1 plots the evolution of policy rate skew over time (blue line) alongside the target federal funds rate (purple line) and the one-year-ahead futures rate (green line)._ The evolution of our measure is largely intuitive: as the economy slows, investors tend to place greater probability on the likelihood that rates will end up lower than projected. As these risks are priced into interest rate options markets, the price of downside interest rate protection rises, and our measure of policy rate skew falls and often turns negative. Upside risks are similarly priced into options markets. For example, policy rate skew was elevated in 2014 and 2021, as expectations for rate increases began to build ahead of the last two Federal Reserve rate hiking cycles. Greenspan (2004) makes clear that policymakers are attuned to these risks as well and have tended to manage such risks by adjusting the path of interest rates, explaining why policy rate skew and the futures rate tend to move inversely.

Chart 1: Policy rate skew tends to lead interest rate cycles

Notes: Chart shows monthly averages of daily data except for the target federal funds rate, which are end-of-month values. Gray bars denote National Bureau of Economic Research (NBER)-defined recessions.

Sources: Board of Governors of the Federal Reserve System and NBER (both accessed via Haver Analytics); CME Group and authors’ calculations.

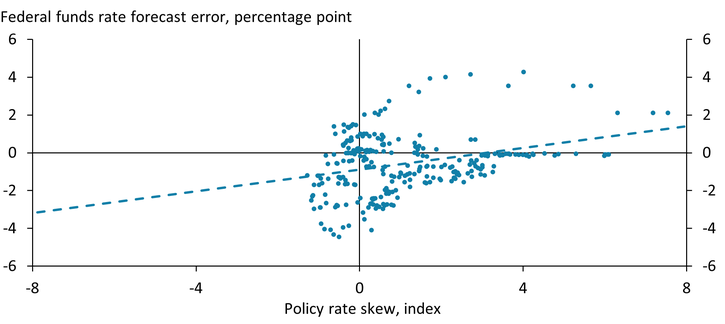

To provide more insight into our measure of policy rate skew, Chart 2 shows the relationship between policy rate skew and private-sector forecast errors for the federal funds rate. The vertical axis measures how the one-year-ahead consensus forecast for the federal funds rate from Blue Chip fairs relative to the realized federal funds rate. Positive values indicate the funds rate was higher than forecast, whereas negative values indicate that the funds rate was lower than forecast. The horizontal axis plots average values of policy rate skew in the days before the BlueChip forecasts were submitted._ The positive relationship in the chart indicates that our market-based measure of policy rate skew captures upside and downside risks to interest rate forecasts. The chart also helps to interpret the magnitudes of policy rate skew: a one percentage point increase in policy rate skew is historically associated with a 30 basis point increase in the forecast error on the federal funds rate.

Chart 2: Policy rate skew helps predict the direction of interest rate forecast errors

Note: Chart illustrates monthly data from January 2001 through June 2023.

Sources: Board of Governors of the Federal Reserve System and Wolters Kluwer/Blue Chip Financial Forecasts (both accessed via Haver Analytics); CME Group and authors’ calculations.

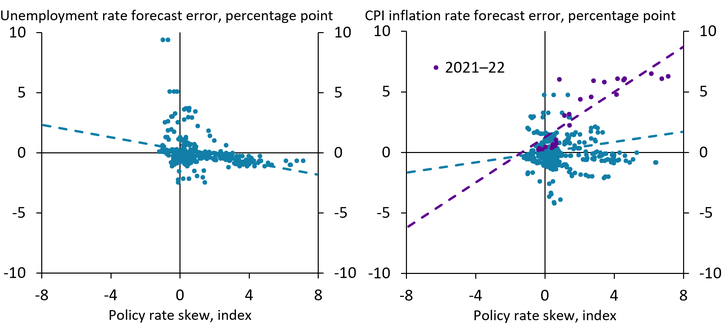

Risks to short-term policy rates captured by policy rate skew are closely related to the outlook for unemployment and inflation. Chart 3 illustrates this linkage by plotting forecast errors for the unemployment rate and inflation (based again on one-year-ahead Blue Chip consensus forecasts) against policy rate skew. As would be expected, policy rate skew has an inverse relationship with unemployment risks. In other words, a negative reading of policy rate skew historically suggests that unemployment will be higher than forecast. In contrast, policy rate skew has a positive relationship with inflation risks. While the relationship between policy rate skew and inflation is somewhat weak before 2020 (blue line), the increase in policy rate skew to record levels in 2021 largely reflected upside risks to inflation (purple line).

Chart 3: Policy rate skew has historically reflected risks to unemployment and inflation

Note: Chart illustrates monthly data from January 1994 through June 2023.

Sources: Board of Governors of the Federal Reserve System and Wolters Kluwer/Blue Chip Economic Indicators (both accessed via Haver Analytics); CME Group and authors’ calculations.

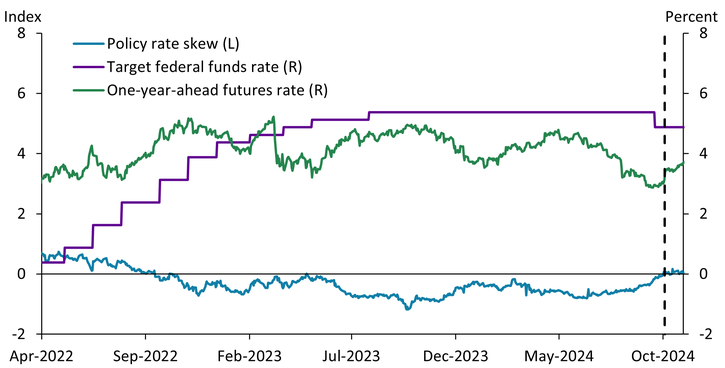

What do our findings imply for the current outlook? Chart 4 shows daily values of policy rate skew since the start of the FOMC’s tightening cycle. From April 2023 to October 2024, policy rate skew was consistently negative, suggesting investors perceived downside risks to the outlook for policy rates during this period. However, on October 2, 2024, stronger-than-expected ADP employment data were released, and policy rate skew turned positive. Two days later, on October 4, 2024, policy rate skew edged higher again after the release of a stronger-than-expected employment situation report from the Bureau of Labor Statistics (dashed line). On that day, the one-year-ahead futures rate moved higher as well, suggesting investors revised their rate outlook higher and expected fewer rate cuts than they did before the release. The increase in the futures path—accompanied by an increase in policy rate skew to near zero—suggests that investors now perceive the risks around this higher rate outlook to be closely in balance.

Chart 4: Policy rate skew has recently increased to near zero, suggesting risks to the rate outlook are closely balanced

Note: Dashed vertical line denotes October 4, 2024, and the release of the Bureau of Labor Statistics’ Employment Situation Report.

Sources: Board of Governors of the Federal Reserve System (Haver Analytics), U.S. Bureau of Labor Statistics, CME Group, and authors’ calculations.

Going forward, our daily measure of policy rate skew can provide a timely indicator of the evolving risks to the outlook for short-term interest rates based on publicly traded options prices. This measure is a useful complement to the Kansas City Fed’s Policy Rate Uncertainty (KC PRU) measure. More concretely, while the KC PRU measures the amount of policy rate uncertainty, policy rate skew measures where that policy rate uncertainty is concentrated across different interest rate outcomes.

Click here to view the KC PRS.

Endnotes

-

1

Specifically, we follow Bundick, Smith, and Van Der Meer (2024) in measuring policy rate skew using the price of options contracts on one-year-ahead interest rate futures from the Chicago Mercantile Exchange (CME).

-

2

Our implementation of the policy rate skew is based on the CBOE white paper “External LinkThe CBOE SKEW Index.”

-

3

We follow Bauer and Chernov (2023), who perform a similar exercise for the 10-year Treasury bond yield skewness measure constructed from option prices on Treasury bond futures.

References

Bauer, Michael, and Mikhail Chernov. 2023. “External LinkInterest Rate Skewness and Biased Beliefs.” Journal of Finance, vol. 79, no. 1, pp. 173–217.

Bundick, Brent, A. Lee Smith, and Luca Van der Meer. 2024. “Introducing the Kansas City Fed’s Measure of Policy Rate Uncertainty (KC PRU).” Federal Reserve Bank of Kansas City, Economic Review, vol. 109, no. 7.

Greenspan, Alan. 2004. “External LinkRisk and Uncertainty in Monetary Policy.” American Economic Review, vol. 94, no. 2, pp. 33–40.

Brent Bundick is a vice president, Taeyoung Doh is a senior economist, and A. Lee Smith is a senior vice president at the Federal Reserve Bank of Kansas City. Alex Gallin, a research associate the bank, helped prepare the article. The Center for the Advancement of Data and Research in Economics (CADRE) provided essential computational support processing and curating the options data used in this analysis. The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.